This week, we’re talkin’ remembering Alan Greenspan and forecasting the new Fed’s actions, where oil/inflation are headed, a Nashville buyers market but with resilient price increases, and I go off on the luddite AI job loss claims.

You won’t want to miss the ending.

Let’s get into it.

Today’s Interest Rate: 6.66%

(☝️ .10% from this time last week, 30-yr fixed)

The Weekly 3 in News:

The Fed held, then turned hawkish, and the chairman wouldn’t sign his own forecast. The FOMC kept rates at 3.50–3.75% in a unanimous vote, but the new “dot plot” erased the rate cut it had projected in March and put a possible hike back on the table. Tellingly, Warsh declined to submit his own dot, because he distrusts forward guidance. (CNBC, Jun 17.) (CNBC)

Housing starts fell off a cliff. New construction dropped 15.4% in May to a 1.18 million annual pace, down 8.7% from a year ago. The tap that fills the future supply pipeline is closing. (Census, Jun 18.) (Census)

Existing-home sales rose, and prices held. Sales climbed 3.2% in May to a 4.17 million pace, with the median price up 1.3% from a year ago to $429,300, the 35th straight month of annual price gains. (NAR, Jun 18.) (NAR)

A Few Fun Things Happening in Nashville This Week

Alan Jackson’s farewell finale at Nissan Stadium, Saturday, June 27. The country legend closes his “Last Call” farewell run with a stadium send-off in Music City. A real bucket-list night, and a reminder that this city’s economy runs on people wanting to be here. (Visit Music City)

Yacht Rock Symphony at Ascend Amphitheater, Tuesday, June 23, 8pm. The Nashville Symphony plays smooth-sailing ‘70s and ‘80s hits on the riverfront. Peak summer-evening Nashville. (Visit Music City)

Dolly Parton’s “Threads: My Songs in Symphony,” multiple dates through June 26.A symphonic celebration of Dolly’s catalog. It is, after all, still Nashville. (Visit Music City)

Remembering Alan Greenspan, and a Hope for His Successor

This week we lost a giant, and we met the new version 2.0, Kevin Warsh.

Alan Greenspan died Monday at 100 (CNBC, NPR). He ran the Federal Reserve for almost two decades, under four presidents, and his record is not without controversy. But I want to honor the part of it that every investor/operator should study, because it is the rarest quality a central banker can have: restraint.

Now, Fed Chair Warsh takes the reins.

The contrast between the two could not be sharper, and it happens to sit right on top of the question every one of us who borrows money is asking: where are rates going?

In the mid-1990s, unemployment kept falling, and the entire economics profession told Greenspan to slam on the brakes. The models said low unemployment had to mean runaway inflation, and the consensus wanted rate hikes to head it off.

Greenspan refused.

He had a hunch that the personal computer and the early internet were quietly lifting worker productivity, raising the economy’s speed limit, which meant the country could grow faster and hire more without prices catching fire. He let the boom run (Brookings). He turned out to be right. Growth averaged roughly 4.5% a year in the late 1990s, unemployment fell to about 4%, and inflation stayed tame (Brookings).

Sit with how lonely that call was. The pressure to act, to look busy, to satisfy the cable-news demand for a response, is enormous. The harder thing, the thing Greenspan did, was to look past the panic of the moment, trust what the data actually showed, and let a good thing keep being good.

Now, Kevin Warsh steps in.

He held his first meeting as chair last week. My hope, and I mean this as a challenge, not a jab, is that he has Greenspan’s spine

Because right now the dramatic instinct and the patient one are pulling in opposite directions, and last week the new Fed appears to have chosen drama.

RIP.

The Fed Flashed Hawkish. Don’t Fret.

Here is what happened, and then here is why I am fading it.

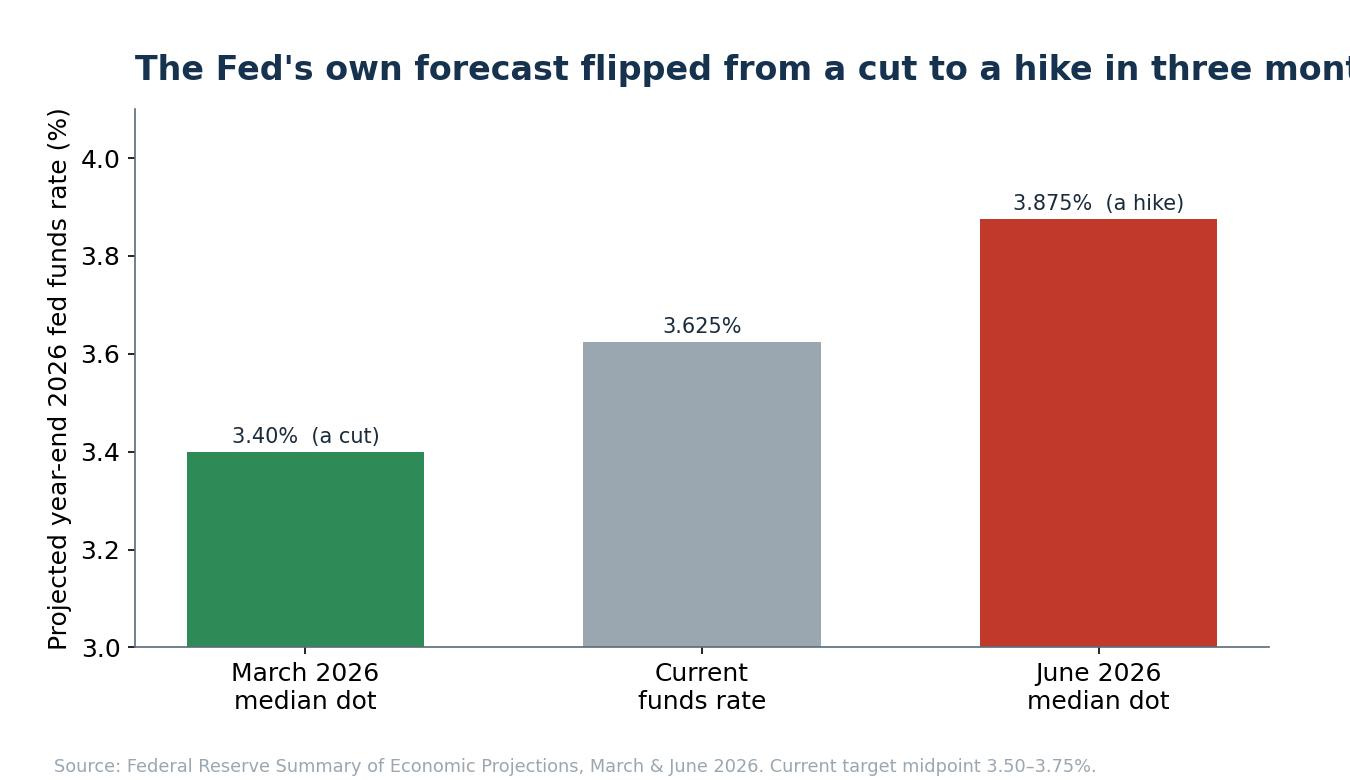

The committee held the funds rate at 3.50–3.75%, which everyone expected. The news was underneath, in the Summary of Economic Projections. In March, the median Fed policymaker still penciled in a rate cut by year-end. Last week, that same median moved up to a 3.75–4.00% range, which implies the next move could be a hike, and the Fed raised its 2026 inflation forecast to 3.6% on headline PCE (Fed SEP, CNBC). Nine of eighteen officials now see at least one hike this year; exactly one sees a cut.

I strongly believe that will NOT happen.

But, fun fact, Warsh, declined to place his own dot on the chart (CNBC).

He has long argued that forward guidance boxes the committee in and makes it harder to change course when facts change, and we now see a chairman who is quietly telling us not to over-read the forecast.

Instead he announced a sweeping overhaul of the institution to get it less involved in the day-to-day of the economy: five task forces to review the Fed’s communications, its balance sheet, its data sources, its work on jobs, and its inflation framework, and he slashed the post-meeting statement to roughly 130 words while abandoning forward guidance altogether. One observer called it “regime change in a velvet glove” (CNBC).

There is a macro backdrop that makes patience the reasonable choice, not the reckless one. The labor market is steady, not overheating: employers added 172,000 jobs in May and unemployment held at 4.3% (BLS). The Fed itself projects the economy grows about 2.2% this year (Fed SEP).

And here is the Greenspan influence that I think Warsh will implement: over the past year, worker productivity rose about 2.8% while unit labor costs rose just 0.5% (BLS). When output per hour grows faster than the cost of labor, you can pay people more and still keep a lid on prices. That is the same signature Greenspan bet on in the 1990s.

The steelman. Sure, headline CPI inflation did hit 4.2% in May, the hottest reading in three years (BLS). Seventeen of eighteen Fed officials judged the risks to inflation as tilted to the upside, and these are people with far more data than I have. So the new chair carries a special burden: if he cuts too early and inflation reignites, he spends his entire tenure fighting for credibility he can never fully win back. From that seat, leaning hawkish would be a reasonable insurance policy, even if it costs the rest of us a little growth. And a hawkish reputation, established early, could itself pull long-term inflation expectations down, which does some of the Fed’s work for it.

So, it you believe May’s 4.2% was the start of something broad rather than an oil spike passing through, the dot plot is not panic; it is prudence.

BUT, I don’t think that is the right read, let me lay out my reasoning.

A Quick Ad Break

Totally shameless plug for my little book. It’s the cliff notes to real estate investing.

Real estate pays you five different ways simultaneously: cash flow, appreciation, loan paydown, tax benefits, and forced appreciation via renovation. Investors who win in choppy markets are the ones who understand they are never betting on just one of them.

Just ~50 pages, and you are ready to rock and roll.

Remember, anyone can build wealth with real estate.

Even you.

The Inflation Scare Was an Oil Scare, and Oil Is Falling

The whole hawkish case in the media and on Wall Street rests on that 4.2% inflation reading. So let’s look at what actually drove that theory.

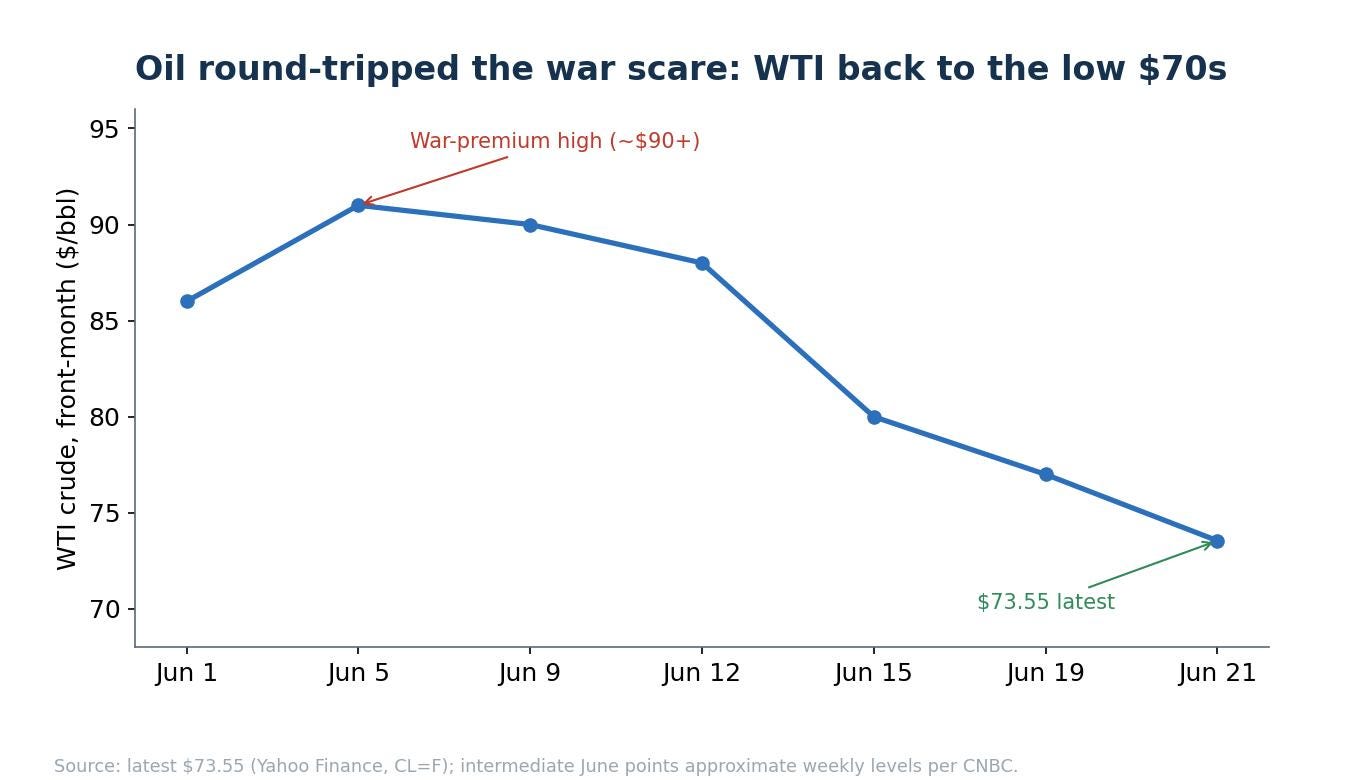

Energy did more than 60% of the monthly inflation damage, while core inflation, which strips out food and energy, sat at a much calmer 2.9% (BLS). May’s inflation was, in large part, a tax imposed by a spike in oil during the worst of the Iran conflict.

That tax is being erroded in real time. WTI crude today has fallen again, back to about $73.55, down roughly 3% on the day I’m writing this and well off the $90-plus levels it touched at the June war-premium peak (Yahoo Finance, CNBC). The energy line that pushed inflation to a three-year high is now deflating, which means the scary headline number may already be peaking.

Households can feel it already.

Consumer sentiment jumped about 9% in June’s preliminary reading, to 48.9, on the back of cheaper gasoline, and Americans’ expectations for inflation a year out fell to 4.6% (University of Michigan). The people filling their tanks are pricing in the relief that the Fed is still discounting. That gap, between what consumers sense and what the committee projects, is the heart of this week’s disagreement.

Anecdote: I filled up today for $3.19 here in TN. Not back to pre-Iron conflict levels but we are now in striking distance.

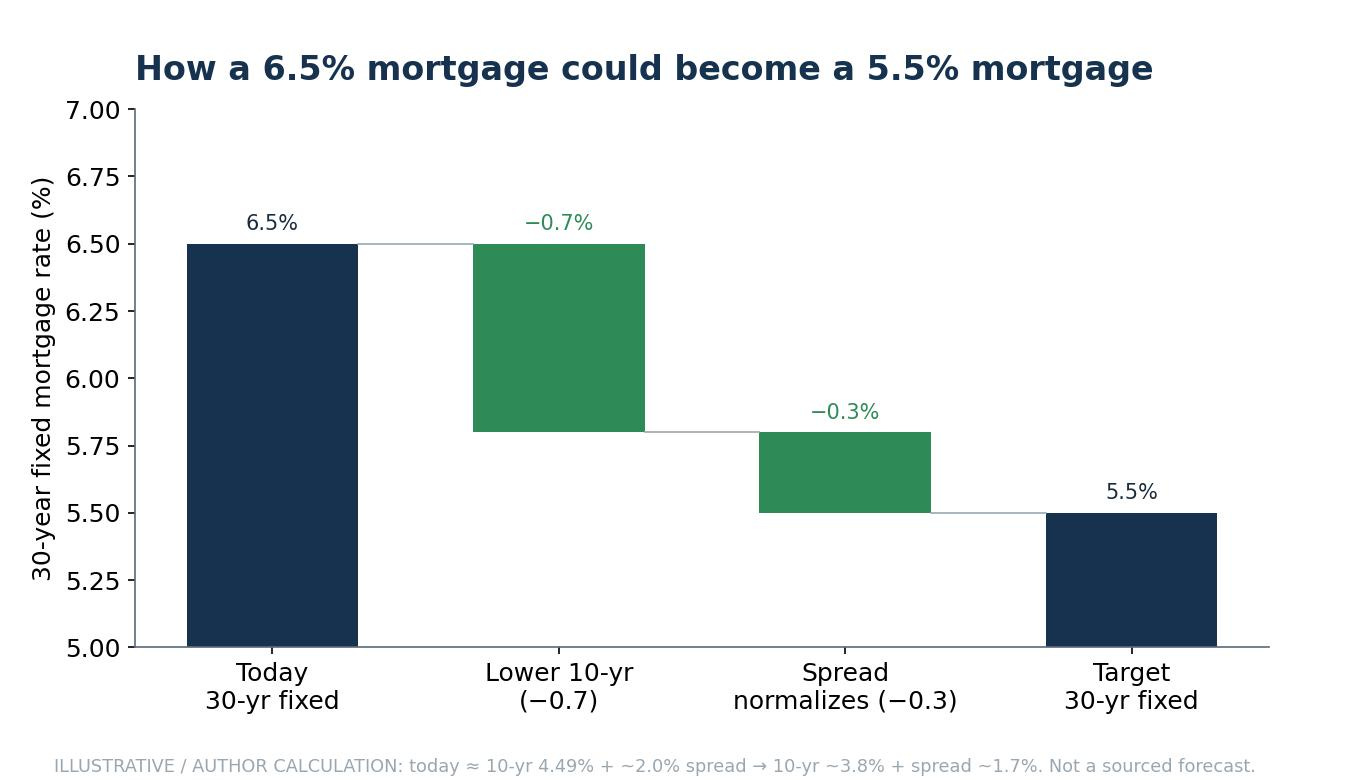

Why the Next Move May Be a Cut, and How We Get to a 5.5% Mortgage

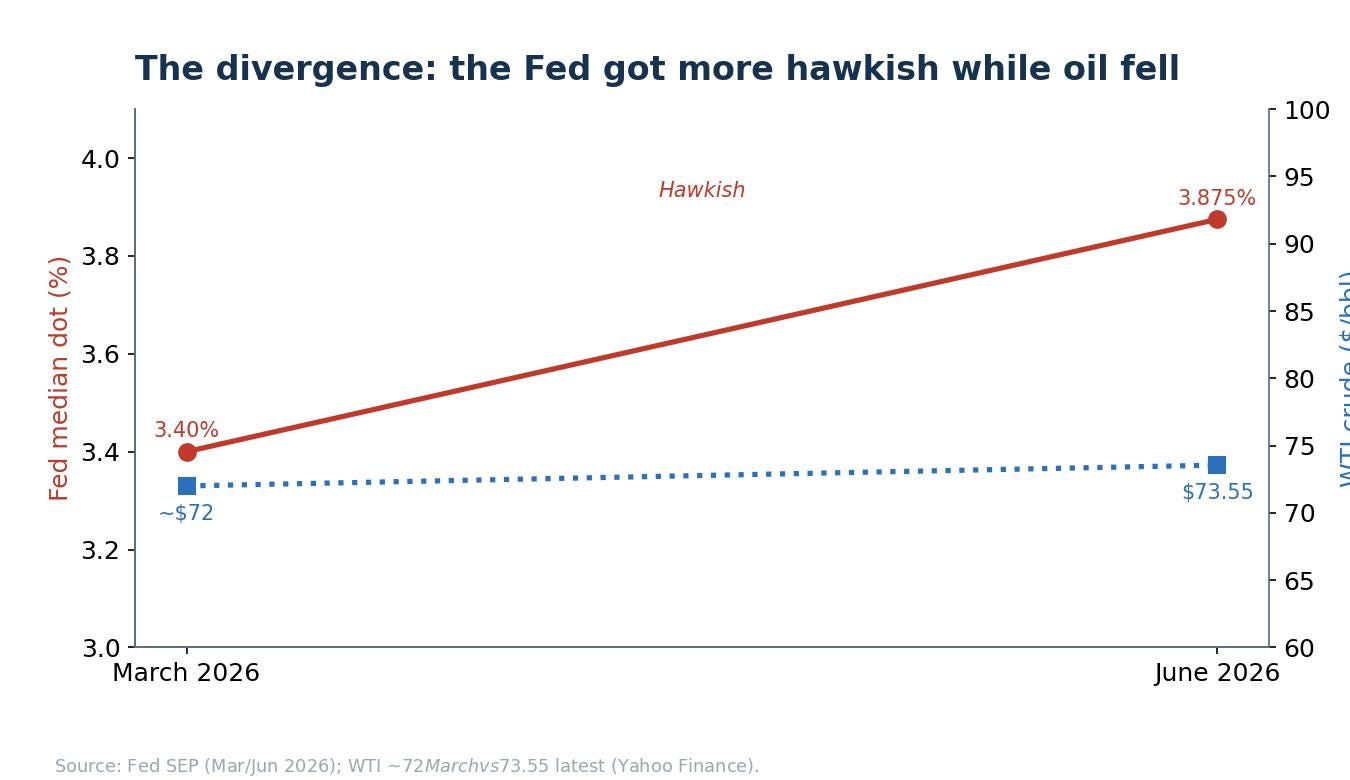

In the span of three months, the Fed’s projected path for interest rates moved up, while the thing that caused the inflation it’s worried about, oil, moved sharply down.

The committee got more hawkish precisely as the case for hawkishness was weakening underneath it.

Consumer inflation expectations fell over the same window. You rarely see the policy signal and the underlying data point in such opposite directions.

The Fed has told us, repeatedly, that it is “data dependent.” If oil keeps fading and pulls headline inflation back toward that calmer 2.9% core, a data-dependent committee follows the data down. That is the path to roughly 75 to 100 basis points of cuts over the next year or so.

Not because the Fed wants to look dovish, but because the numbers will eventually give it no reason to stay this tight.

Here is the part that matters for your portfolio, and the part most media outlets get backwards. The mortgage rate you pay does not come from the Fed funds rate. It tracks the 10-year Treasury yield plus the spread that lenders add on top. So the road to a meaningfully lower mortgage runs through two levers,

Neither one requires the Fed to do anything dramatic.

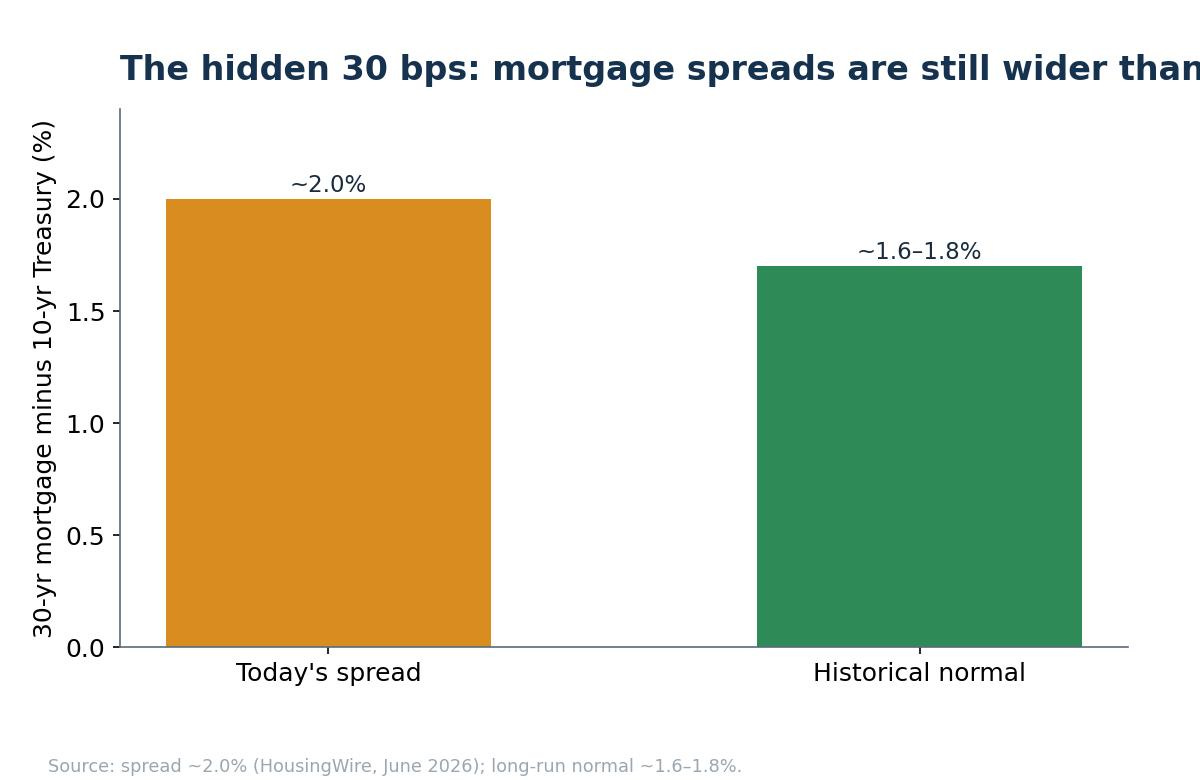

Today, the 10-year sits around 4.49% (CNBC), and the spread between the 30-year mortgage and the 10-year is running near 2.0%, which adds up to roughly today’s 6.5% rate. The catch is that this spread is unusually wide. Historically it runs closer to 1.6–1.8% (HousingWire). That gap is not permanent. It widens in times of fear and uncertainty, and it narrows as conditions calm.

So here is the arithmetic.

If disinflation resumes and the Fed eases, the 10-year could drift toward something like 3.8%. If the spread normalizes toward 1.7%, we add those together and we land near a 5.5% 30-year mortgage. Two gentle, plausible moves, neither one heroic, and the headline number that governs affordability drops by a full point.

You can already see the early appetite for this.

Even with rates near their highs for the year, refinance applications were running about 20% above year-ago levels in late June, as borrowers with older, pricier loans moved to lock in the current ones (Mortgage News Daily / eciks summary). And demand on the purchase side is levitating higher, not collapsing: existing-home sales rose 3.2% in May (NAR), even as new construction fell 15.4% (Census).

I believe demand will continue to rise, while the future supply pipeline thins.

If rates then ease toward 5.5%, you have buyers with a fresh reason to act meeting a market that built fewer new homes to sell them.

But, hope is not a strategy

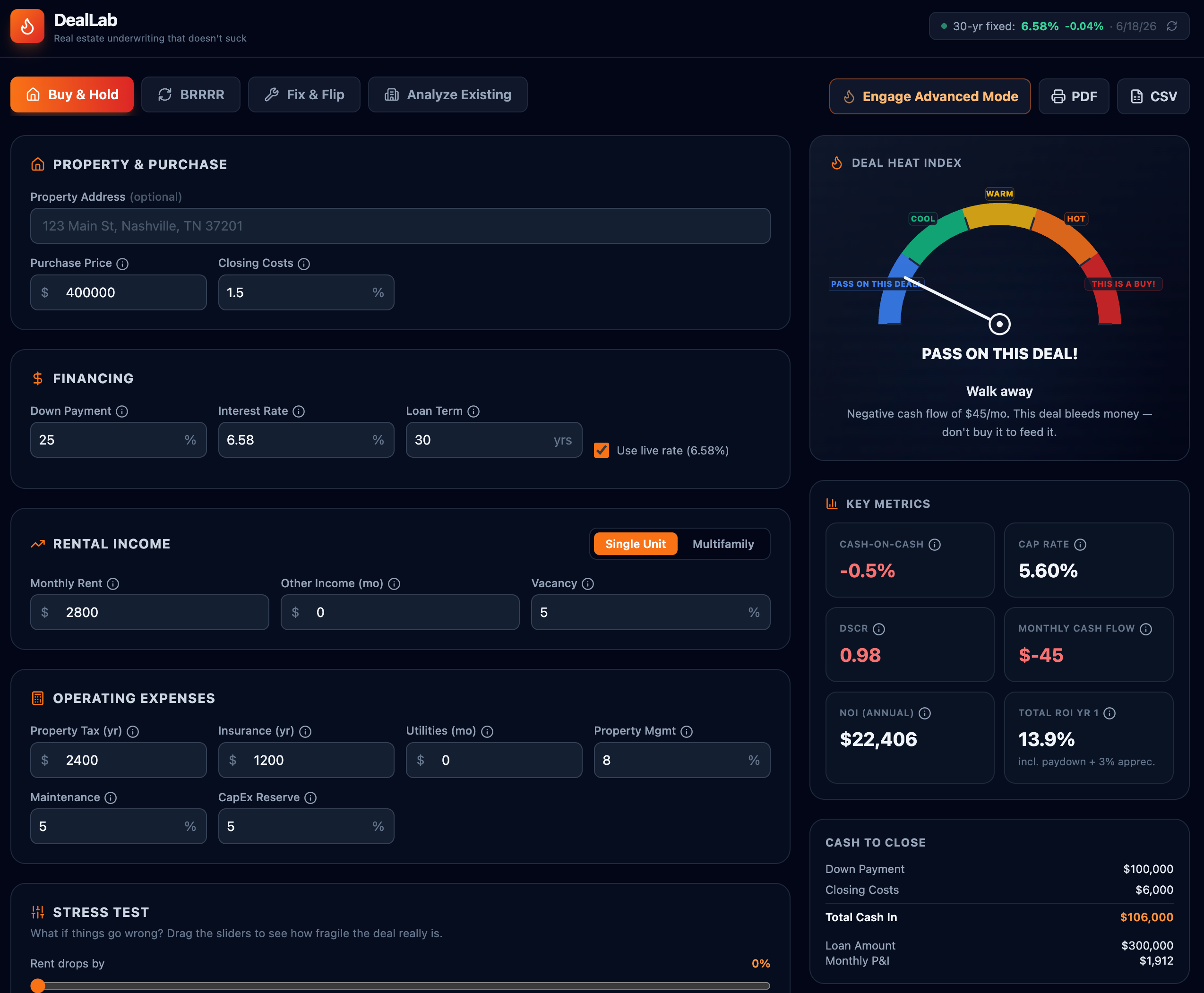

This is exactly the kind of environment where doing your own underwriting separates real investors from the posers.

A deal that doesn’t pencil at 6.5% but sings at 5.5% is not a deal you buy today on hope; it’s a deal you model both ways, so you know your margin of safety before you sign. Real estate builds wealth through several engines at once: cash flow, appreciation, loan paydown, tax benefits, and leverage. When the appreciation story gets loud, as it is now, the cash-flow math is what keeps you solvent while you wait for it. (If you want the long version of that framework, it’s the whole premise of my book.)

So, remember to run your numbers tight. Need help? I built a free deal analyzer so you can underwrite any rental, BRRRR, or flip in seconds, with live mortgage rates, cap rate, cash-on-cash, DSCR, and a deal “heat score.” Model your next deal at 6.5% and again at 5.5% and watch what a single point does to your returns.

Plus, I just added Advanced Mode for the pros who want to get into the weeds. It’s in beta, so kick the tires and tell me what to fix or add. Feel free to bookmark it; it’ll come in handy later. 👉 nashvilleinvestoragent.com/deal-analyzer

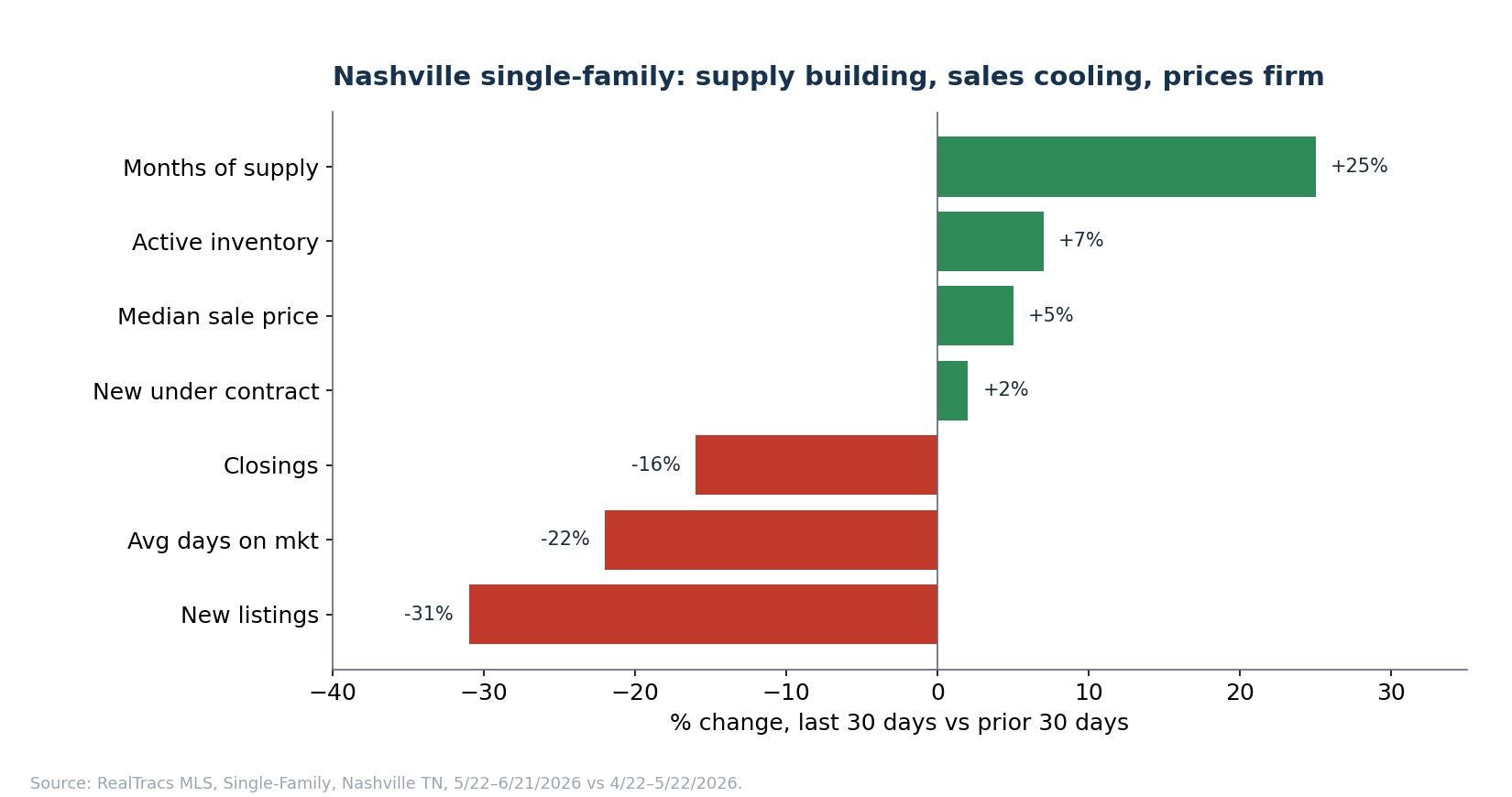

Nashville: The Market Quietly Tilts Toward Buyers

In my home market of Nashville, the data tells an interesting story: inventory is tilting towards buyers but prices are still creeping up.

Months of supply jumped 25%, to 5.23 months. New listings fell 31%, and closings dropped 16%. At the same time, the median sale price actually rose about 5%, to $665,400 (source: RealTracs MLS, Residential Single-Family, Nashville, TN, 5/22–6/21/2026). So we have an interesting setup for the second half of 2026: fewer homes trading hands, inventory accumulating relative to that slower pace, and sellers holding on their sales price.

This split is fascinating, and could only be true in a resilient market that we have here.

Why?

Business are expanding here and jobs are plentiful.

Unemployment remains far below the national average (3% vs 4.3%).

For an investor, this setup presents a future opportunity. Make sure this is the case in your target city.

Because, a market with accumulating supply and more patient buyers is one that springs to life when mortgages cross the 6% rubicon and head toward 5.5%.

I give it 12 months, absent another middle east side quest by our lovely government.

This is why, for me, I’m a voracious buyer today. I’m looking over the horizon for what 2027 will look like. And so far its low supply, higher rents, fewer deals to be had.

My Skeptical Take

I’d like to touch on a little something different. AI fear over job loss.

First, some history.

In February 1961, TIME magazine ran a piece called “The Automation Jobless.” with the subtitle: “Not Fired, Just Not Hired.”

Sound familiar?

“The election of President Kennedy in 1960 intensified the focus on technological unemployment. The Kennedy administration took automation concerns more seriously than its predecessor, with the US Secretary of Labor warning of workers being left on a "slag heap." 1961 would see Time Magazine publish an article titled ‘The Automation Jobless’ and predictions were made that automation would end most unskilled jobs. One professor predicted counter revolution (PA).”

The country had 5.4 million people out of work, the Labor Secretary had just convened a special panel to study the threat, and a respected expert was quoted calling automation “the nation’s second most important problem.” First, he said, was peace. Second was the machine (TIME, Feb 24, 1961).

The evidence looked obvious. In the chemical industry, production jobs had fallen while output soared. Steel was making far more with thousands fewer workers. And the line that ought to stop every doom-monger cold: on the farm, the article noted, one man could now grow enough to feed 24 people, where in 1949 he could feed only 15 (TIME).

The experts looked at all of it and concluded the economy had finally run out of room to put people to work.

Here is what actually happened.

1961 began one of the greatest job-creating stretches in American history. The labor force roughly doubled in the decades that followed. The farm and factory work they feared losing did largely vanish, and it turned out to be one of the best things that ever happened to the American worker, because we did not run out of jobs, we ran out of those jobs, and built new ones the 1961 experts could not have named.

The fear of new technology and and job loss has repeated time and time again.

Heck, it may be the single most reliable pattern in economic history.

“In a 1922 commencement speech at Wellesley College, President of the Rockefeller Foundation - Raymond B. Fosdick pondered: “Can education run fast enough” for people to beat the machines. A number of books would be written regarding the subject. ‘Social Decay and Regeneration’ - published in 1921 - would be reviewed by the New York Times, who asked ‘Will Machines Devour Man?’, accompanied by an provocative illustration of someone being fed into a sausage making machine (PA).”

The New York Times asked “Will Machines Devour Man?”

In the 1930s, Keynes coined the phrase “technological unemployment,” while Henry Ford countered that for every job a machine takes, it creates many more. In 1955, President Eisenhower waved off the automation panic, noting it had “plagued people for 150 years and always proved groundless.” In 1965, Peter Drucker wrote a piece titled, plainly, “Automation Is Not the Villain.” In 1995, Jeremy Rifkin published The End of Work, at almost the exact moment America began posting its best employment numbers in a generation (Pessimists Archive).

It seems like every generation produces a confident class of luddite forecasters, who count the jobs a new technology will obviously destroy, but forget to count the ones it will create.

Nassim Taleb, who has built a career pointing at the emperor’s wardrobe, or lack thereof, is less polite about that crowd than I would be:

“Those with brains no balls become mathematicians, those with balls no brains join the mafia, those with no balls no brains become economists.”

The man has a point.

The people most certain about the future tend to have the worst record of predicting it, and a credential on the wall doesn’t fix the batting average. We moved from an agrarian economy to an industrial one to a manufacturing one to a service one, and at every handoff the smart money swore the music was about to stop.

It never did.

The pie did not get carved into thinner slices. It got bigger, and there turned out to be more than enough for everyone willing to step up to the table. (I came to a similar conclusion a few weeks ago, when I argued that AI may be adding jobs rather than destroying them.)

I don’t say this to dismiss the risk. It is real, and it lands on real people; the worker who is “not hired” is not a statistic to the family living it. But there is risk in everything, even crossing the street. I see great optimism for AI and can hold two things in my head at once: 1) technology displaces specific people in specific roles for a short time, and 2) it has expanded the overall economy, without exception, for two centuries, and will continue to do so.

Anyone telling you this time the machine finally wins is selling the same forecast that has been wrong since the spinning jenny.

And that is exactly how I read AI.

The automation panic, the end-of-work panic, and yes, the inflation-can-never-come-down panic all rest on the same four words from Sir John Templeton, who made a fortune buying precisely when everyone else was sure the world had changed for good, named them:

“The four most dangerous words in investing are: ‘This time it’s different.’”

Alan Greenspan understood this in his bones.

In the 1990s, the whole industry, and much of the body politic, told him a hot economy had to mean runaway inflation, and he had the nerve to trust the productivity data instead and let the thing run.

We lost that man this week.

My hope is that his successor remembers the lesson: that the patient call, the one that looks past the noise of the moment, is usually the hard one, and usually the right one. The oil scare fades, the inflation panic ages as badly as the automation panic did, and the rate normalizes.

That, I think, is the trade worth making, made with your eyes open to the ways it could be early.

P.S. If you want a smart, hopeful book to put that whole pattern in perspective, I’d point you to “The Rational Optimist” by Matt Ridley — the definitive, readable case that human ingenuity keeps expanding the pie. Perfect fit for this essay; reads like a recommendation, not a sales pitch. Amazon link.

—

Need some personal help with your real estate portfolio?

You can consult one-on-one on the phone with me, The Skeptical Investor!

Get professional advice from someone who actually owns, operates, and brokers real estate. Not just some partner in a fund making money off others.

Want to Grow? - Get clarity on how to grow your business or scale.

Stuck? - Get answers to your problem, let’s hop on the phone and figure it out.

No "guru" trying to sell you an expensive course. No BS. No fluff. Only results.

I'll give you my frank, brutally honest advice. Book a call with me today.