Take Your Mortgage With You? Portable vs Assumable Loans.

Why keep your low interest rate and just hot swap the underlying asset? Well its complicated.

Today’s Read Time: 6 minutes

This week you get TWO! Articles.

You luck ducks.

Why?

I’m doing a little travel in Deutschland and Türkei! Back in the Nashville saddle in 1.5 weeks. So next week you will get a break from my insights, inferences, implications, ideations and, or course, rantations.

This week, we’re talkin’ Fed interest rate cut, and I dive deep on assumable and portable mortgages. Like really deep.

Let’s get into it.

Today’s Interest Rate: 6.36%

(☝️ .02% from this time last week, 30-yr mortgage)

The Weekly 3 in News:

Lumber Prices Continue Downward. Lumber futures are trading around $535–546 per 1,000 board feet. Way, way down. -12% over the past month and year. For comparison, the peak was $1500/bf in 2021.

Former Fed governor Adriana Kugler resigned from the central bank after preparing to submit financial disclosures for 2024 that Fed officials could not certify because they included several prohibited activities, including: buying individual stocks (not allowed), moving in and out of those stocks within weeks (not allowed), doing so in FOMC blackout periods (not allowed). Yet Congress can still do all of the above. Yuck (WSJ, Timiraos).

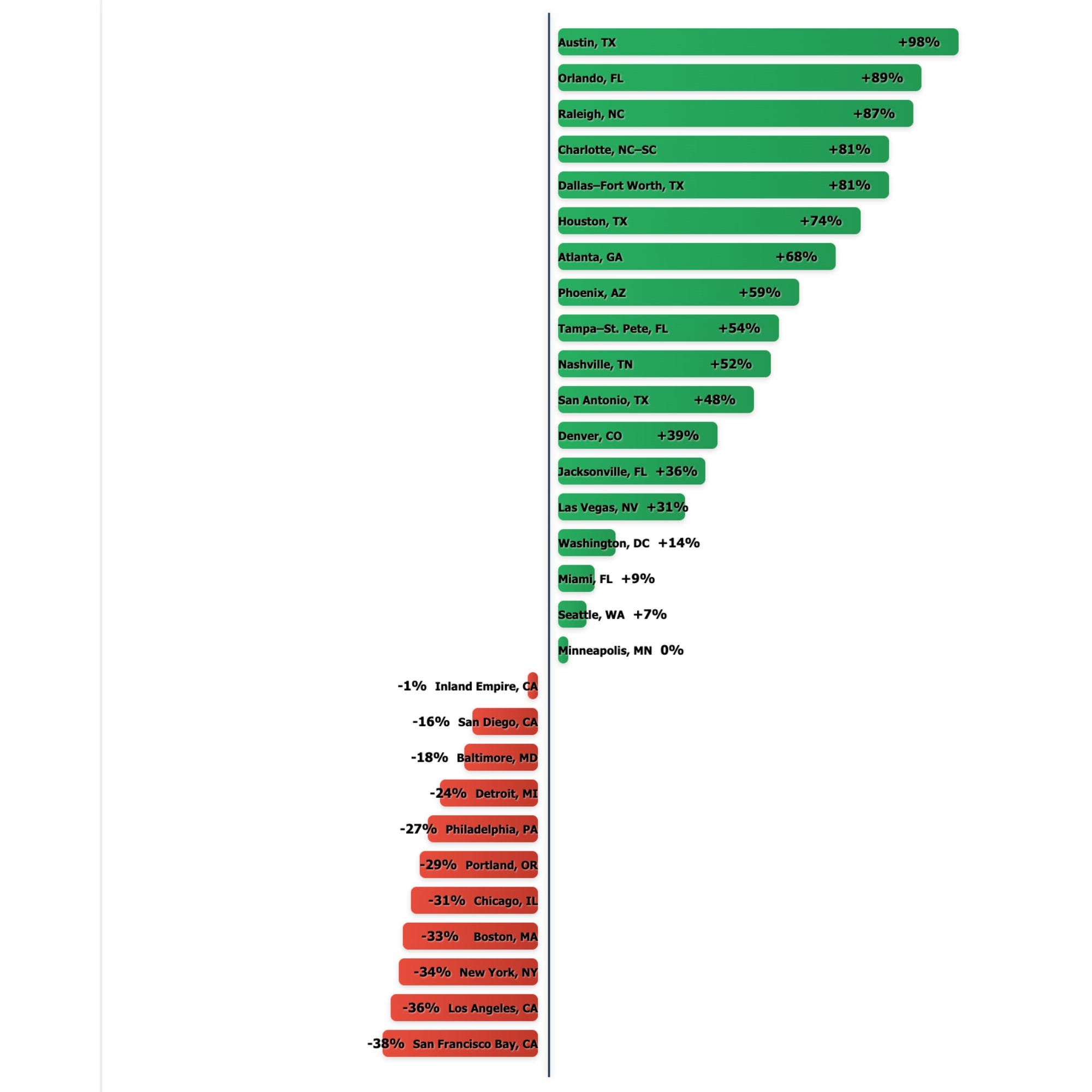

Nashville News - Nashville is Baby Booming! Not only have folks been flocking to Nashville to make a new home, they have been putting the bedroom to good use. The children under 5 population has exploded in Nashville, up 52%! A boon for future growth. And take a look at the other big winners: Austin +98%, Orlando +89%, Charlotte +81%. And losers: SF -38%, LA, -36%, and NYC -34%. Not coincidently, the growth cities below are also where the most housing has been built, and the opposite for those shrinking. (Fijan).

In other words, Build Housing = Make Babies.

Über-Quick Fed Rate Cut Update:

We FINALLY got a jobs report yesterday, Yay! Which showed… well, it wasn’t totally clear. If you are a bear or a bull, Democrat, or Republican, there was something for everyone to hate and love in this report.

In short:

The economy grew +119,000 jobs, beating Wall Street analysts’ whisper expectations by 2x! BUT the trend is stagnant since April with little net growth. And 119k is a low-ish historical number, the average since 1980 is 126k.

Unemployment held at 4.4%, up a tick (.12%) from some forecasts and rising gradually from 4.1% a year ago. Labor market appears to continue cooling. This number is what was expected.

We got more negative job revisions of (god, we are bad at estimates), downgrading the jobs we thought we had created in prior months.

Job gains were mostly in health care and food services, while transportation and warehousing saw losses.

Payrolls are continuing to grow faster than inflation, but growth itself is weak, and has shown little net change since April 2025 (aka stagnant, not expanding meaningfully).

The only real problem? This was September’s data.

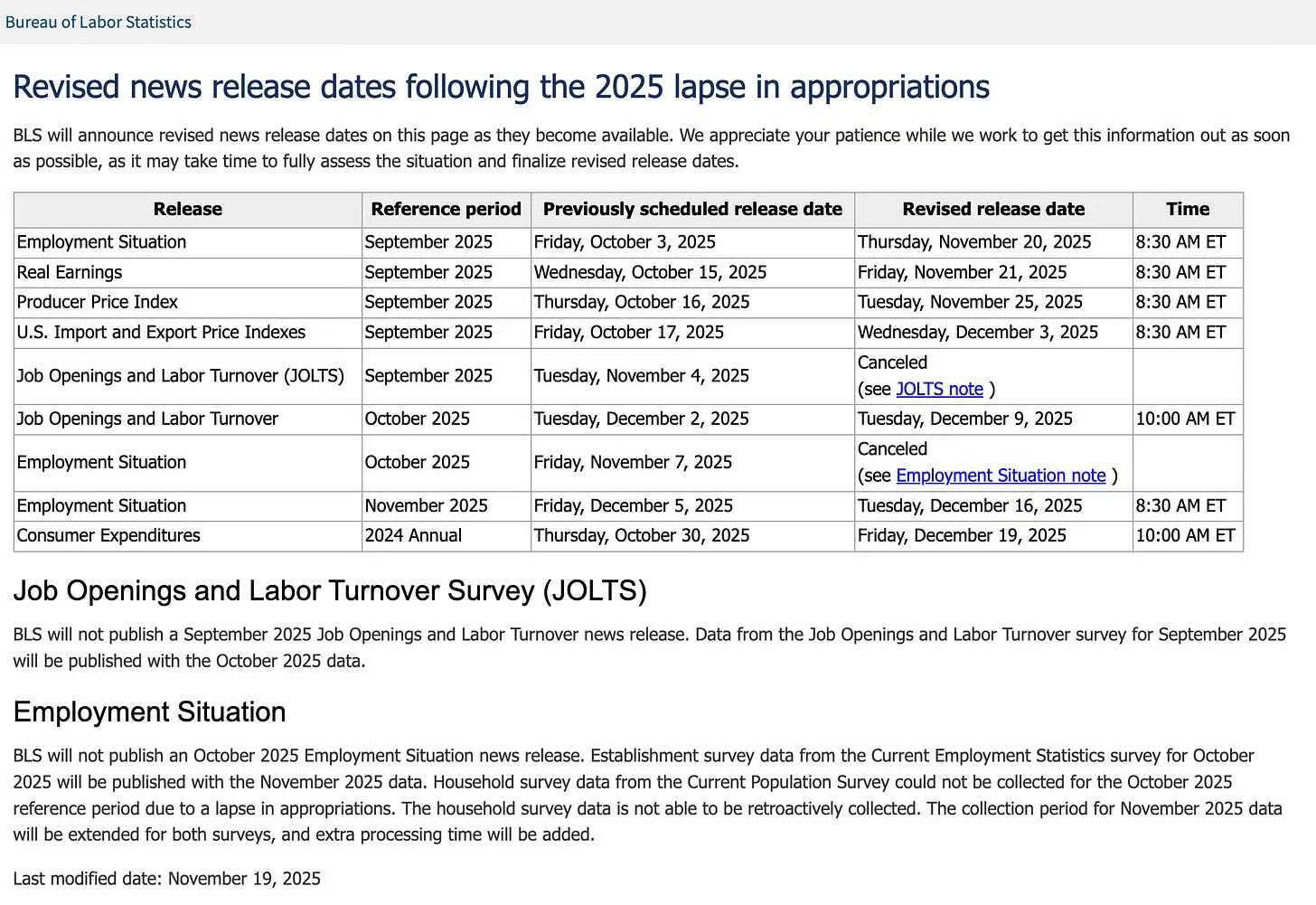

The second problem? (Ok I lied…) There won’t be another jobs report until after the next Fed meeting on Dec. 9-10 to determine whether or not to cut interest rates.

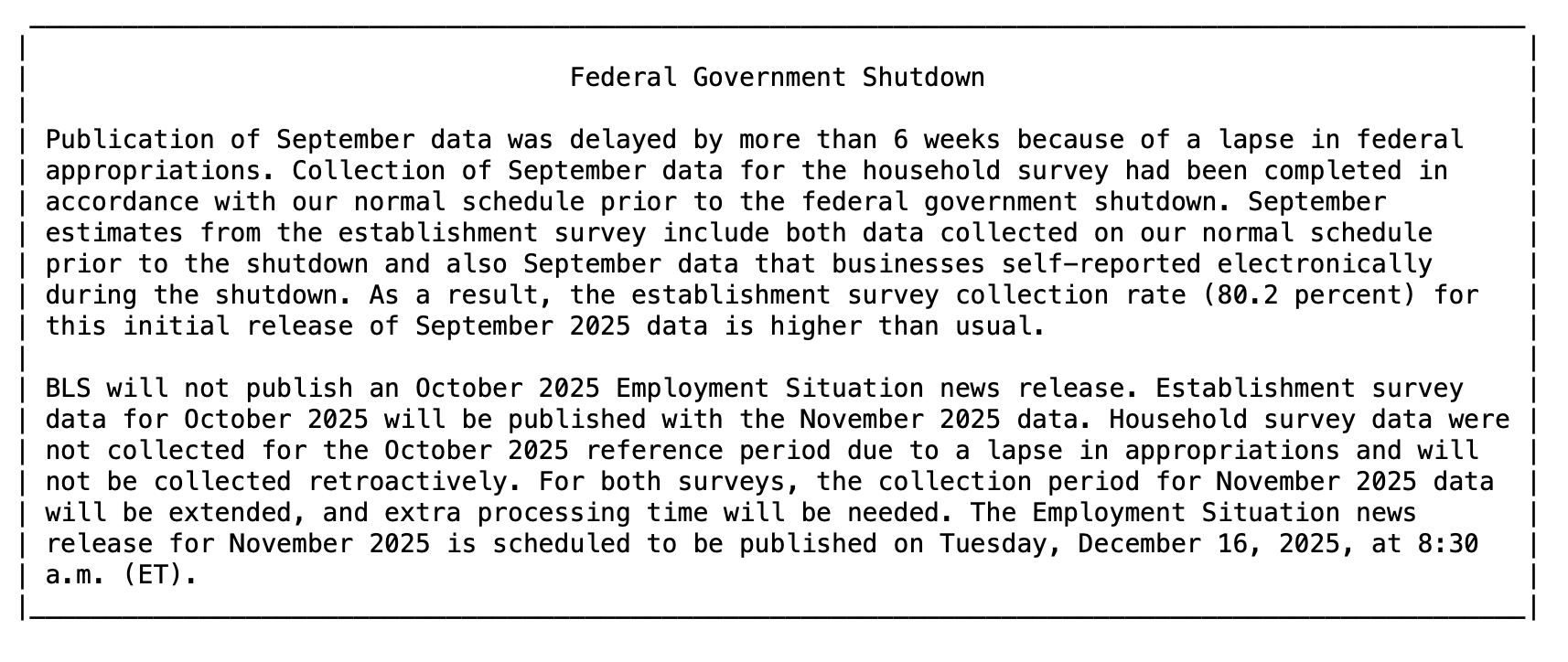

The BLS cancelled the October jobs report, and the November report won’t be published until Dec. 16, all because of the Government Shut Down.

The job openings/quits report (aka the JOLTS) for September is also cancelled. The Oct JOLTS will be published Dec. 9, so the Fed will have that just in time (they do get it a bit early tho) (Fed).

Does the Fed have Enough Data for the December Decision?

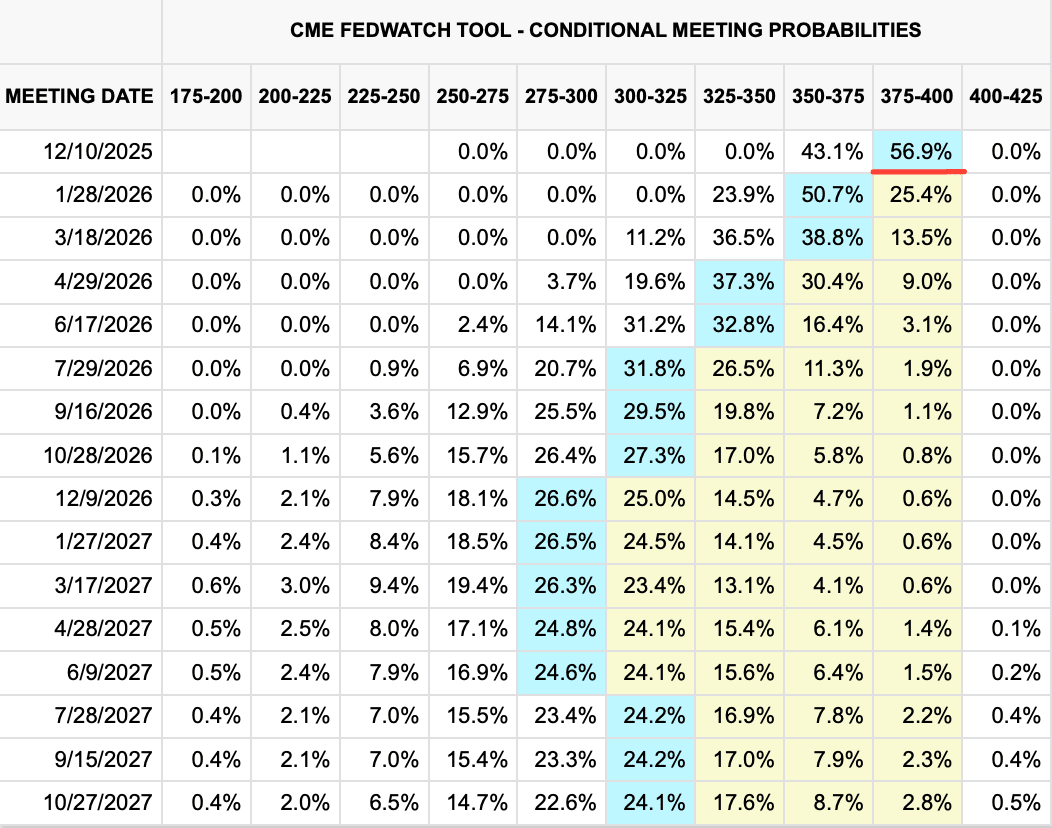

Now, to be fair, Fed officials have reiterated that they have enough information to do their job forecasting the economy and making interest rate decisions without this gov data. I’m skeptical, and the market agrees. Probabilities of a Dec rate cut fell on this news of “data decay.”

The Bond market is pricing in a 43.1% chance of a rate cut (56.9% no cut). This was the reverse just a few days ago.

The betting market too has flipped in recent days, now showing a slightly lower chance (32%) of a rate cut (66% no rate cut) (Polymarket).

Big Change Since Yesterday

The volatility in the stock market has spooked people. Just yesterday, the numbers were worse: Bond market was pricing in a 31.8% chance of a rate cut (68.2% no cut). Bettingmarket had a chance (28%) of a rate cut (69% no rate cut) (Polymarket).

What a difference a day makes.

Why Did This Happen?

Well, unless you were living under a rock - which I sometimes do, no judgment, it’s nice and cool - Congress was unable to fund the government for the start of the Oct 1st fiscal year and we were forced to endure a government shutdown for 43 days, which ended on Nov 12th.

From the BLS:

The Bureau of Labor Statistics (BLS) staff were furloughed during this time. So they could not survey, tabulate, and analyze jobs data. And the report could not legally be published. The Establishment Survey and Household Survey were the primary sources of data, which could not be performed.

This is Why We Need Better Data

In my view, this only highlights the need for higher-fidelity reports from the private sector, not based on surveys but on real-time data from businesses.

It is a little ridiculous that we still rely on person-to-person surveys (literally 60,000+ phone calls) that must be performed to know how the labor market and economy are performing. What if Amazon needed to survey shoppers to know what sold on their platform, instead of software tracking it automatically?

We would think that is insane.

Well, that’s pretty much what the BLS still does.

Why not use software to capture real-time data? Why not contract to private industry operators to get anonymized / metadata? Why does this take thousands of BLS employees to perform these reports like a typewriter from when my parents were in middle school?

The entire process is antiquated and needs to go!

But I digress…

Ok, let’s switch gears to some related news: portable mortgages. Another way to keep interest rates and transaction costs down.

Portable and Assumable Mortgages?

Recently, Federal Housing Finance Agency Director Pulte made news when he said the agency was looking into allowing/facilitating mortgages that are portable.

So, what the heck is a portable mortgage? And what is this assumable mortgage I’m also hearing more about now?

A brief primer:

Assumable Mortgages

Want to buy a home?

Great, interest rates are ~6.3%. Yuck.

But the current owner/seller has a 3% mortgage, can I have that?

Oh, well it… no. Well…maybe. But, it depends.

Do they have an FHA / VA loan backed by the government? Then yes, you can you can assume that loan and that loan and get that %! Just pay us an $1800 assumption fee and the down payment.

If not, no. You have to get a new loan at current rates. And pay us a new loan origination fee (typically .5-1%).

The seller does not, they have a traditional, conventional loan.

Sorry, no dice.

In other words, an assumable mortgage is just that. In general, you can take over someone else’s loan, pay the bank (or title company) a down payment to replace the equity the homeowner has in the home (and/or a second mortgage if need to replace a large % of equity a homeowner may have), who, in turn, provides that to the seller so they can go on their marry way. FHA loans allow assumptions and charge an $1800 fee to do so.

Again, this is possible today, but only on certain kinds of existing home loans. Need help finding homes that have assumable mortgages? There is an app for that.

Check out Roam (not a sponsor). Most of the homes are basic starter homes, but it’s actually pretty cool.

Portable Mortgages

Have a mortgage on your home?

Want to buy a new home?

Well, getting a new loan involves considerable transaction costs and, because of the zero-interest-rate policies of 2020-2021, most folks have mortgages with interest rates in the 2-5% range.

So, if I already have a loan on my current home, can I just keep that loan and swap the asset that secures that loan, from my current home to the home I want to purchase?

If your mortgage was portable. You could!

But alas, it is not. Sorry.

:( …

A Quick Ad Break…Cash App

Make your paychecks work for you

When you set up direct deposit with Cash App, you can get paid up to 2 days early. That means less planning around payday, more living on your own schedule.

And that’s just the start

Put a percentage of every paycheck toward savings, stocks, or bitcoin*

Keep all of your money with no monthly or hidden fees

Make your money go further with 3.5% interest** on savings and up to $200 in free overdraft coverage***

Know your money protected by 24/7 fraud monitoring and built-in security features

Want to advertise to the more than 30,000+ weekly readers of The Skeptical Investor? You can! Advertise with us; we can help you grow your business. Reach out.

Ok, back to business.

The Case for a Portable and Assumable Mortgages

The core pitch: Most buyers are sellers, and vice versa.

If you’re locked into a 2.8% rate from 2021, why sell and jump to 7%?

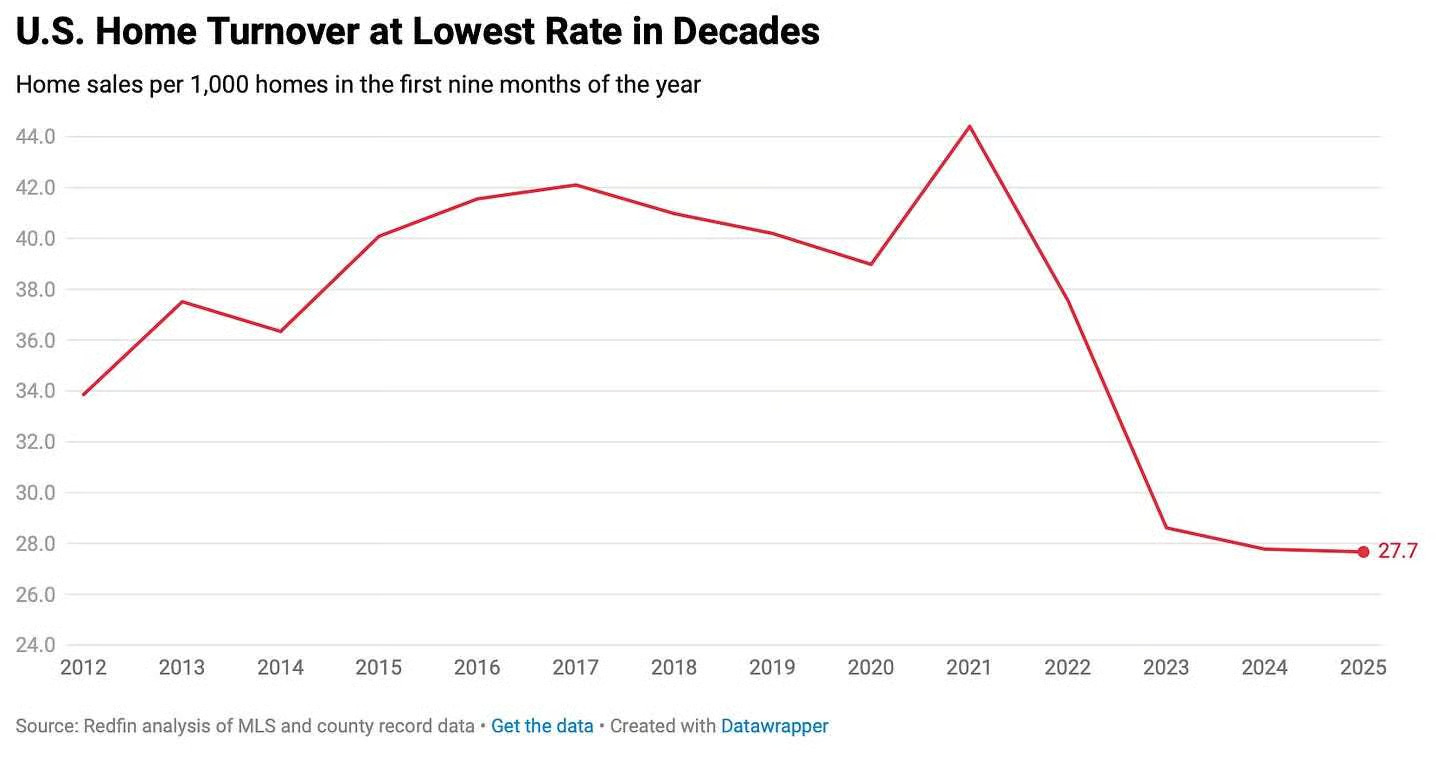

That hesitation is killing existing home supply—only 28 out of every 1,000 homes changed hands in the first nine months of 2025, the lowest turnover in decades per Redfin.

Portable/assumable loans would let you get far better terms so you can move were you want or upgrade to a better place, freeing up your old home for others.

The hope?

More existing inventory hits the market, easing the crunch for first-timers and boosting overall sales. Sure, inventory is higher today than last year, but we are still not back to normal. And in places like my home market of Nashville, that inventory is mainly new build/basic starter homes not value-add existing homes / multifamily we investors need. In fact, there is a dearth of existing homes for sale.

And in aggregate, including new households forming, we’re still short millions of units nationwide, with estimates around 4-5 million deficit (RedFin). This could help unlock some movement without waiting for massive new builds.

The Monthly Payment is King

Even if more homes flood the market, unaffordability stays high with high prices and rates. The median home price is $420k, up 2.2% year-over-year, per NAR. Inventory might rise, but without rate relief for new borrowers, it’s not a game-changer for entry-level folks. Rates are still at 6.3% and will likely levitate from here, as I have recently written about.

Assumable mortgages are a little tricky. Because a buyer wants to take over the loan from another person, who has a different credit rating, different savings amounts, different debt amounts, etc… their risk profile/actuary is different and thus, the bank should be allowed to charge an assessed amount and % rate based on the risk to the bank that the borrower defaults. Allowing all homebuyers to assume mortgages could then lead to a banking/housing crisis a la 2008 GFC. There is good reason to only allow this on loans that are already government-backed in case of default so as not to spread throughout the banking sector. As is done today. However, allowing a specific subsector of homebuyers to assume mortgages and providing government backing could make this an option for some, but not all. FHFA Director Pulte is “looking into this” but I bet they instead focus on less economically risky portable mortgages.

Speaking of which, the portable mortgage. These would be more viable. The buyer has already been qualified for the loan, already has the loan, and has been paying that loan every month (assuming they are in good standing of course). They are known to the bank as creditworthy. So why not allow them to hot swap the underlying asset that the loan backs from one home to another?

And if the new home is a higher price/more valuable, the buyer could simply put down more $ to secure the loan (or get a second mortage, if they qualify) and ensure the homebuyer has 20%+ equity in the new home, which a bank will want in case they need to default (note: there are also different types of portable mortgages, so this is a simplified process).

Portable Mortgage: The Case.

Well, if it wasn’t obvious, we are in the third year of the lowest home sales ever, driven by interest rates that are 2-3x what they were in 2020-2021.

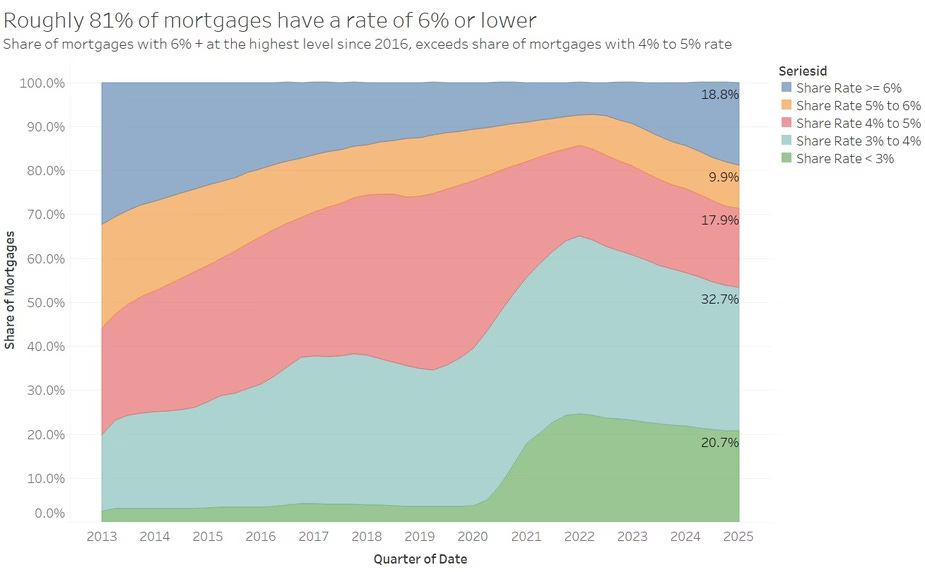

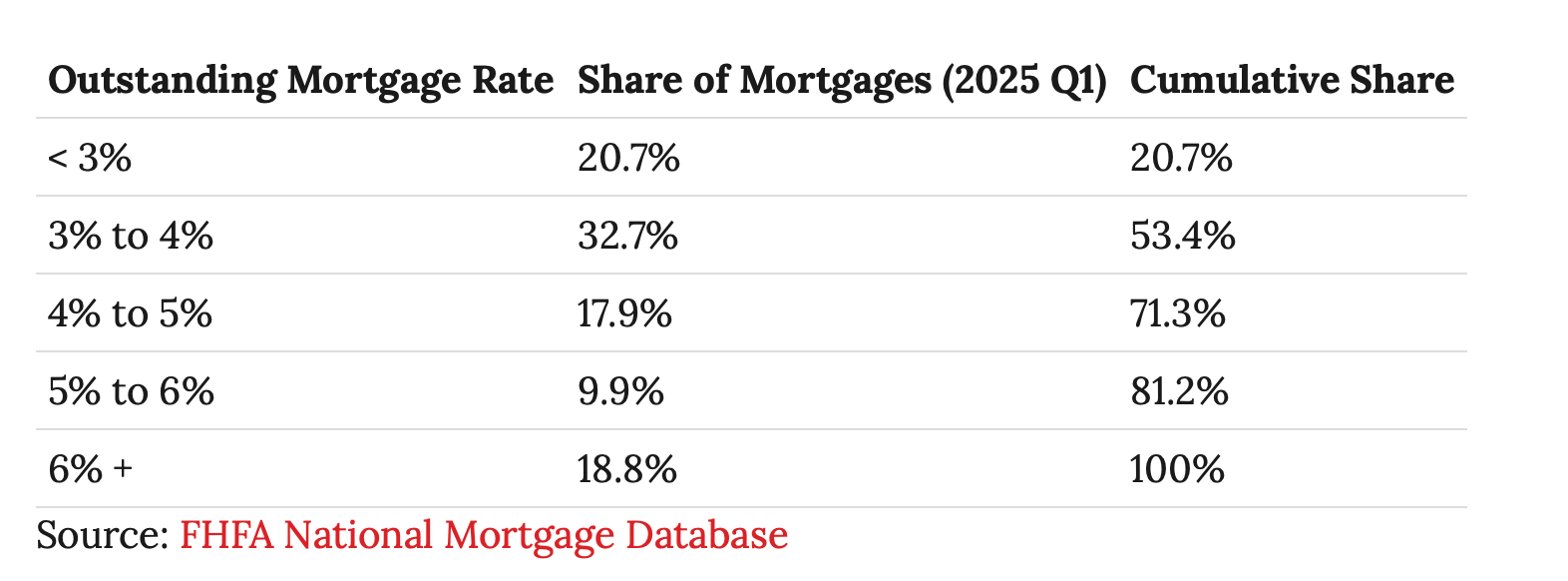

And because of that zero-interest-rate policy of 2020-2021, most homeowners with a mortgage have one of those low interest rates. 81% have a rate lower than 6%.

Every Tom, Dick, and Harry refinanced in 2021 to a low rate.

And 71.4% have a rate 5% or below!

Again, most buyers are sellers, so allowing them to take their mortgage with them is a very attractive prospect and would incentivize both demand and supply of existing homes

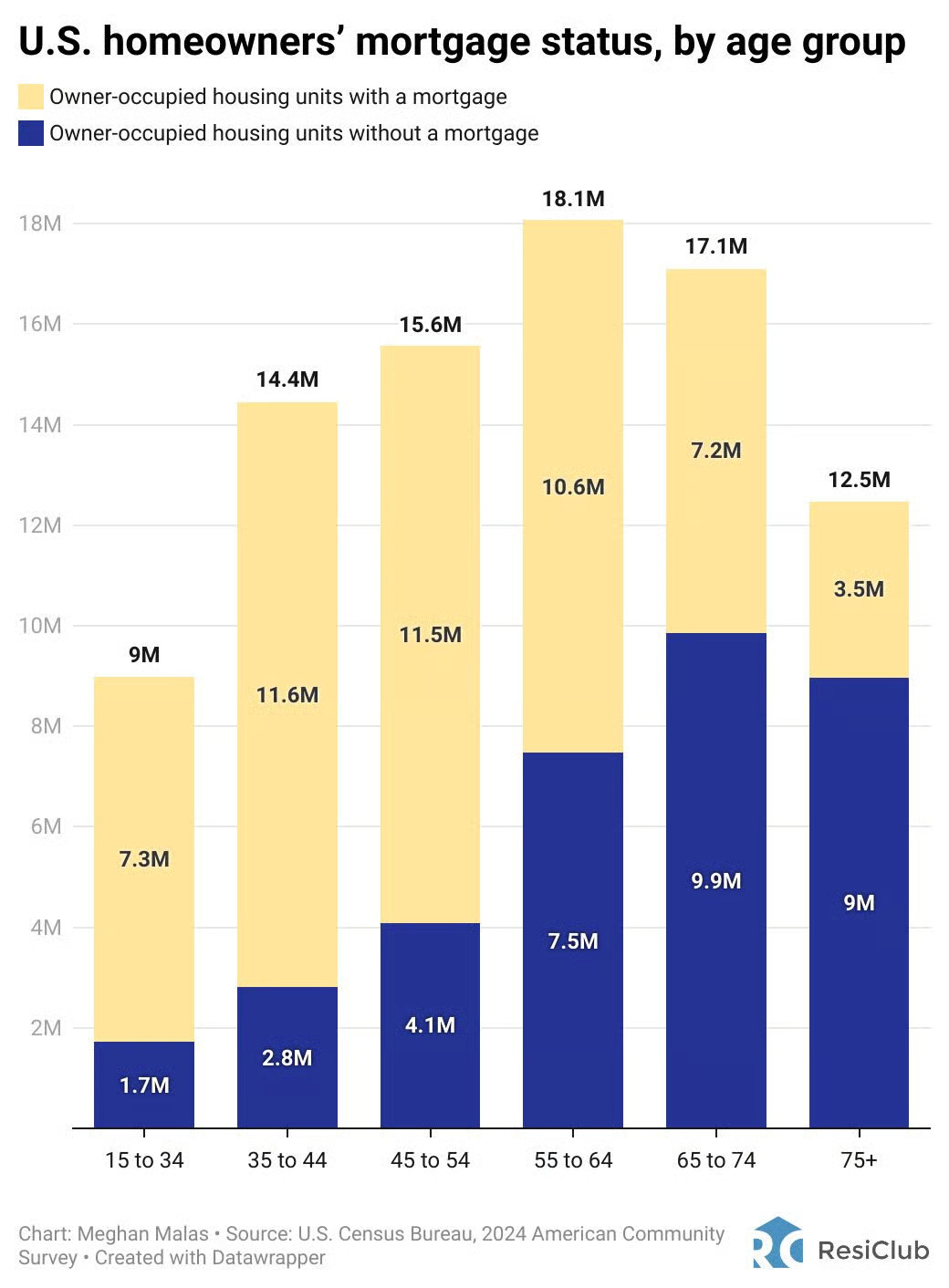

Yes, yes, I know many homeowners don’t actually have a mortgage on their home. 40.3% to be exact. They own it outright. So they couldn’t take advantage of this if they decide to move. But then again, they have no mortgage…

Bigger Issues for Lenders

This is where it gets ugly. Lenders price loans assuming an average life of about 7-8 years—not the full 30 on the mortgage —because most folks sell or refinance their loan in that time period (fun fact, this is also why mortgage rates track the 10-yr Treasury (NOT the Federal Reserve Funds Rate), they are competing assets sold to investors on the secondary market as Mortgage Backed Securities and 10-yr Treasury bonds).

Portable mortgages could stretch that closer to the full 30 yr term, sticking banks with low-yield loans as rates rise. Think 2% interest when markets’ at 7%—that’s a loss-maker that could strain bank balance sheets or even lead to failures without bailouts. Importantly, another result would be low bank liquidity to make new loans, as fewer investors would buy MBS if the interest rate were so low.

To offset, lenders might hike rates upfront for everyone, worsening the housing mess.

And here is why Director Pulte is talking about Portable Mortgages.

As the head of Fannie and Freddie, he wields the power to buy these loans off bank balance sheets so they can then make new loans to others (at the prevailing higher rate). And Fannie and Freddie don’t care as much if the return is 2-5%. They also could allow for a portable mortgage fee, as they do with assumable mortgages.

One issue: technically, doing so would violate the Qualified Mortgage law, so a new regulation would have to be put in place. It is unclear if Congress would be needed for that, or if the Administration could do so by decree (as is their preferred method of cutting through red tape).

My Skeptical Take:

As my dad used to say: “Things are good!”

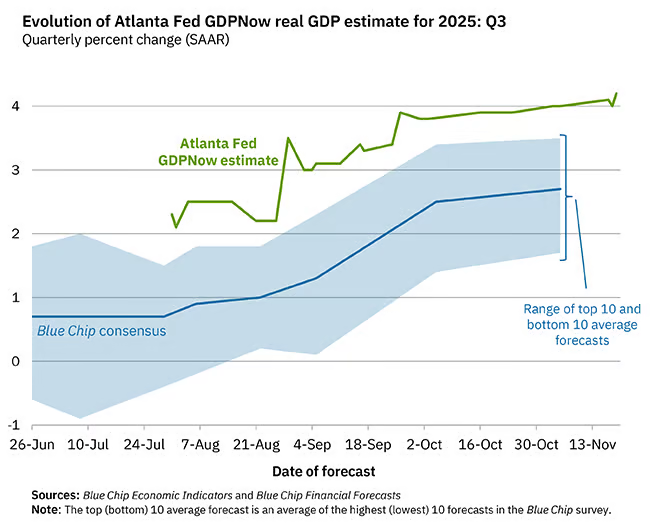

The Fed itself sees the economy growing like gangbusters. The Atlanta Fed is just out with their GDP predictions for this quarter three and, things are (still) looking good.

Q3 is expected to grow real GDP growth at 4.2%, up .1% in just a few days.

How about Interest Rates?

It is difficult to tell how the September jobs report will affect a seemingly fractured Federal Reserve FOMC board when they vote in December.

I do think they will cut .25% BUT, as the bond and betting markets are telling us, that is no longer to be expected.

One anecdote: another Fed Governor announced his retirement last week, adding fuel to the rate cut chances in the Spring.

Bostic will be retiring in the new year, removing another less dovish member from those who decide interest rates. Bostic actually used to be a mild dove (pro-growth and favoring lower rates), but has become more hawkish during this Administration. Unfortunately, his stance change appears to have been more political than data-driven. Good riddance.

This retirement is expected, but nonetheless, it will drive more enthusiasm at the Fed come Spring in favor of more dovish/pro-growth and lower interest rate monetary policy.

And a new 2026 Fed voting member, Philadelphia Fed President Anna Paulson, just publicly signaled her dovishness, saying “[she supported cutting rates at the last two meetings and remains] a little more worried about the labor market [than inflation.]”

She also noted, “Historically, when job gains are concentrated in acyclical sectors like healthcare, that is a precursor to a slowdown.”

Bullish for more rate cuts in 2026.

But, count my skeptical ears perked for further labor market cooling.

Rate Cuts: When A Portable Mortgage Makes Less Sense

I LOVE the idea of a portable mortgage.

Keep reading with a 7-day free trial

Subscribe to The Skeptical Investor Newsletter to keep reading this post and get 7 days of free access to the full post archives.