Forget Inflation. Watch the Labor Market.

Inflation is priced in, labor will drive interest rates from here.

Today’s Read Time: 11 minutes

This week, we’re talkin’ April inflation report ran hot at 3.8%, the bond market freaked out, mortgage rates whipsawed back to 6.65%, and the Fed-cut path got priced out.

I’m taking the other side.

Plus — the details on Nashville’s largest development project ever, The Oracle Development.

Let’s get into it.

Today’s Interest Rate: 6.65%

(☝️ .23%!! from this time last week, 30-yr mortgage)

Bond market sold off hard after the April CPI/PPI prints. Three weeks ago we were at 6.40%. Last Friday at 6.42%. This Friday at 6.65%.

The Weekly 3 in News:

Both April inflation reports were hot. CPI was 3.8% and PPI (aka wholesale producer prices) was 6.0%, YoY — the hottest reading since May 2023 and March 2022, respectively. But, importantly, energy is doing 40%+ of the move as core inflation, taking out volatile food and energy prices, held at 2.8% YoY. Nevertheless, the market saw the headline and panicked. (BLS, May 12)

Homes Are Selling. US pending home sales rose 9.6% year-over-year in the four weeks ending May 10, reaching their highest level since 2022 — declining mortgage rates in Jan-April may have pulled buyers off the sidelines, but mortgage rates already climbing back to 6.65%. Yet, a tighter supply, with new listings down for a third straight week should help keep inventory relatively suppressed (see below for more). (Inman/Redfin)

Businesses are Building. March core capital goods orders jumped 3.3%, the biggest gain since 2020 and far above the 0.5% consensus. Capital goods orders are a leading indicator of business investment, a strong signal that companies are committing capital driving GDP growth (this is likely also from pull-forward orders ahead of expected price hikes from the Iran conflict (Reuters).

A Few Fun Things Happening in Nashville This Week

Trace Adkins at the Ryman — Fri May 22 & Sat May 23, 8 PM. Two nights of late-spring country at the mother church. Carolyn Dawn Johnson opens Saturday. The kind of Ryman weekend that reminds you why people moved here in the first place. (Ryman)

The Agency Nashville’s “Executive Landing” launches. Announced May 12. A concierge relocation service targeted at HNW corporate transferees and execs moving to Middle Tennessee. Very COOL! The capital is moving in, and so are the people. (Morningstar PR Wire)

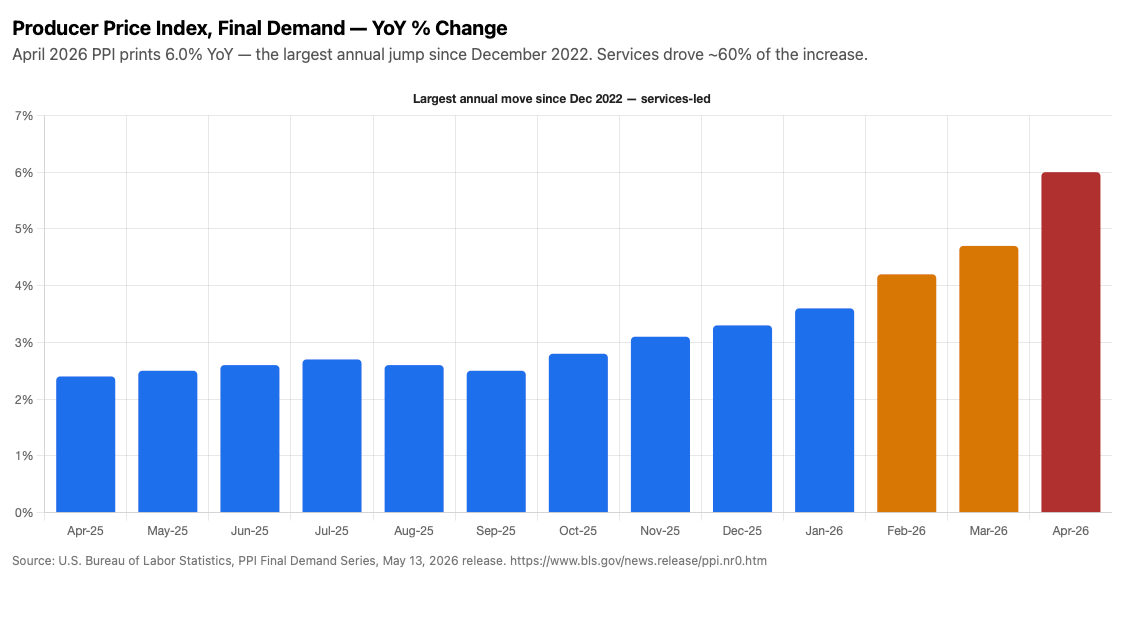

Producer Prices Are On The Rise

The market freaked this past week. Inflation is on the rise once again.

If CPI was the data point that grabbed the headlines this week, PPI was the data point that should have, IMO.

April producer prices rose 1.4% in a single month — the largest monthly jump since March 2022, the deep tail of the original inflation wave. On a year-over-year basis, the index rose 6.0%, the largest annual move since December 2022. Roughly 60% of the increase came from services. The core measure — excluding food, energy, and trade services — was +0.6%. (BLS, May 13)

This is the problem: What rolls into PPI today rolls into CPI tomorrow. Core inflation (ex food, energy, trade) ran +0.6% in a single month, which says the producer-side stickiness is not just an energy passthrough. Services prices could be accelerating into a softening labor backdrop.

For us in real estate, the PPI matters in two specific ways.

First, the materials and labor cost stack for anyone who builds, renovates, or maintains.

Second, the PPI is what insurance companies look at to price next year’s homeowners and commercial insurance premiums. Replacement cost to rebuild your home is a PPI-driven number. Florida, California, Texas operators saw their premiums double in 2024-2025 and are still recovering.

Watch those insurance premiums.

And yet… the inflation PPI surprise is largely an energy story, which is a Strait of Hormuz story.

Strip energy and the picture is relatively muted — core PPI is +0.6% on the month, which is hot but not catastrophic. Services prices in PPI have historically been a noisy series, and you can find single-month jumps of this size every couple of years that don’t roll into anything durable. The hottest single piece of services PPI in April was wholesale margins — not wages, not productivity. Margins are mean-reverting. So this inflation report is probably an energy-plus-margin spike, not a structural reacceleration.

Counter-counter point: that’s true if WTI cooperates from here. If WTI sits above $100 through summer, May and June PPI will be uglier than April.

Counter-Counter-Counter point: keep reading…(I’m more worried about the labor market).

A Quick Ad Break….ResiClub Housing Analytics

Running numbers on a new deal or determining what market to invest in?

Real estate investors and Realtors alike need data.

Ener ResiClub Terminal—A powerful new platform that brings together housing market data, analytics, and insights at the metro, county, and ZIP Code level.

Whether you’re evaluating a new deal, modeling housing demand, tracking investor activity, or advising clients, the ResiClub Terminal helps you make faster and informed decisions.

Check out the ResiClub Terminal here!

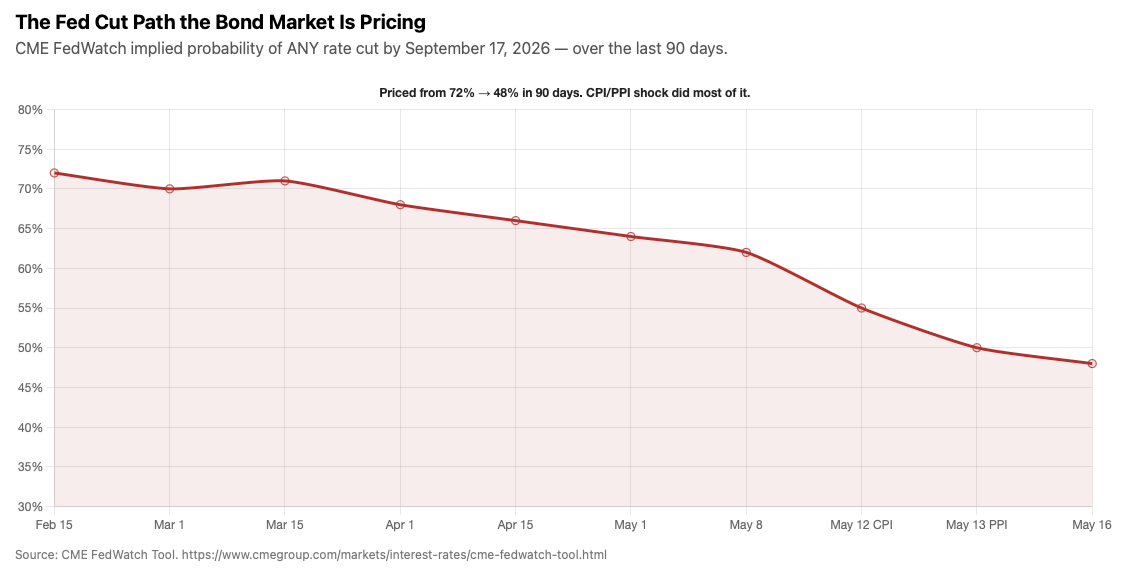

The Bond Market May Be Offsides.

In my humble opinion, the next move by the newly refreshed Federal Reserve will be a cut in interest rates based on the labor market’s status, not inflation.

This is not consensus, which right now is:

Inflation reaccelerated. The Fed is on hold. Warsh is incoming and he’s a hawk. Rates higher for longer. No cuts in 2026. Could even be a hike.

Polymarket has 0 Fed cuts in 2026 at ~70% implied probability.

CME FedWatch shows similar: the June meeting at >98% no-interest rate change, and September cut odds at ~48%, down from ~70% two weeks ago. (CME FedWatch).

That collapse happened in 4 days, almost entirely on the CPI and PPI reports.

The market repriced from “the cut path is alive” to “the cut path is dead” on two data points that both have a single shared driver, energy and its passthroughs.

I think the market is offsides.

A re-read of Ben Graham’s classic book The Intelligent Investor may be in order.

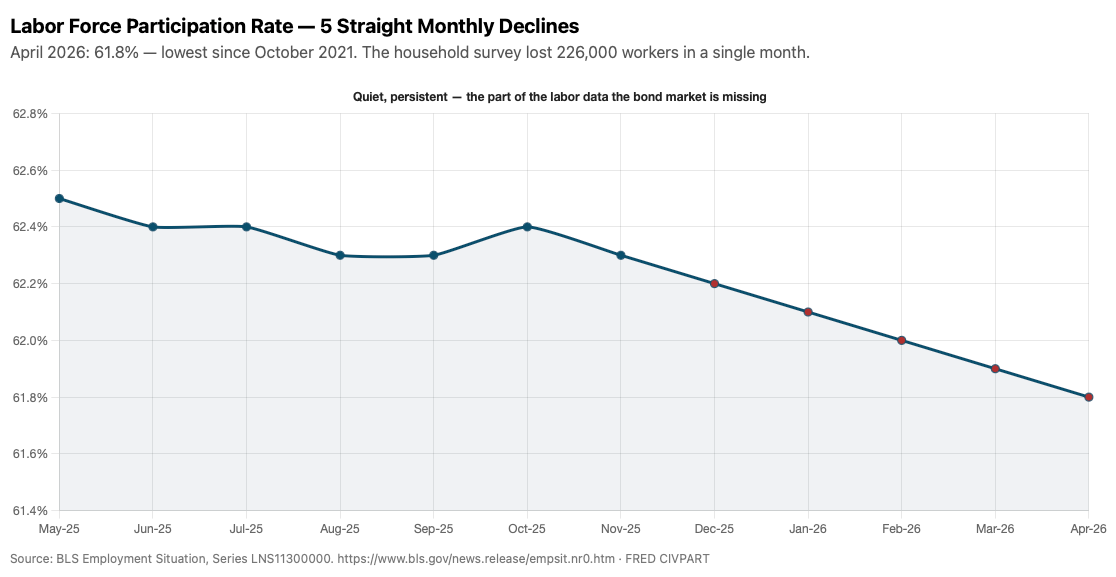

The Labor Market May Be Quietly Weakening

Headline unemployment held at 4.3% in April. The headline payroll print was +115,000 — a “beat” against +55K consensus. The market read those two numbers, said “labor’s fine,” and went home. (BLS, May 8)

The market may be is wrong. Look at the second derivatives.

Labor force participation fell to 61.8% in April, the lowest reading since October 2021, and the fifth straight monthly decline. (BLS) The household survey lost 226,000 workers in a single month. The Fed and the bond market love to point at the aging-demographics explanation for participation declines, and that’s part of the story, structurally. But a 5-straight-month decline of this slope is not demographics. It is people who used to be in the labor force, looking for work, no longer looking. That’s not a tight labor market. That’s a labor market where searches are getting more discouraging.

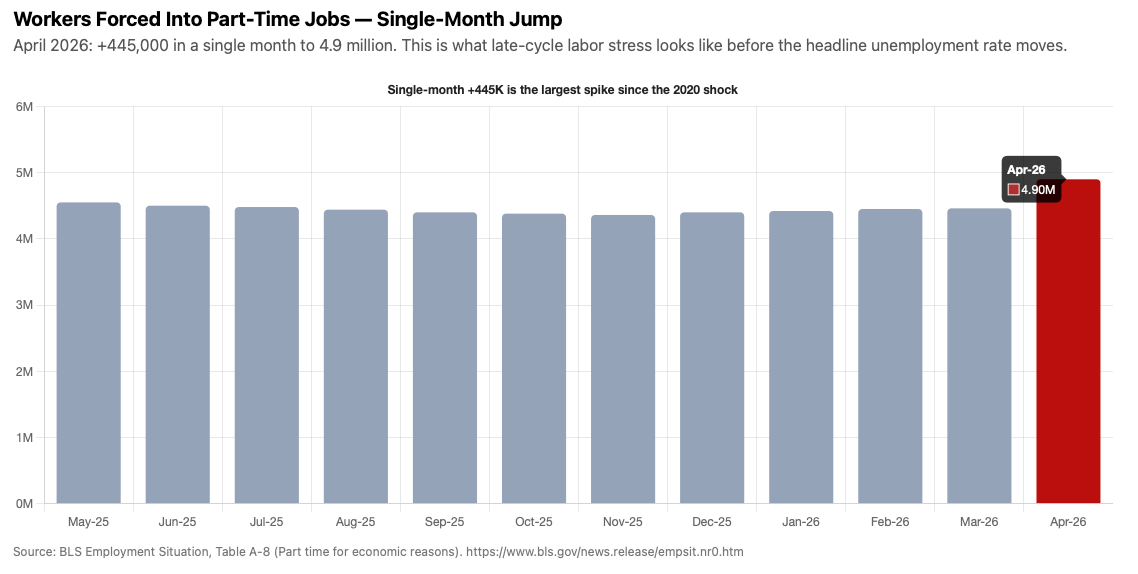

Now look at the part-time number.

The number of people working part-time for economic reasons — meaning they want full-time work but cannot find it, or their hours got cut — jumped +445,000 in a single month to 4.9 million in April. (BLS, Table A-8) That is the largest single-month spike in this series since the 2020 pandemic shock. Outside of pandemic data, you have to go back to the 2009 recovery period to find moves of that size. This is what late-cycle labor stress looks like — before the headline unemployment rate moves. Hours get cut. Full-time gets converted to part-time. Then the layoffs come, and only then does the U-3 unemployment rate spike.

JOLTS, the most lagging of the lagging indicators, showed hiring jumping to 5.6 million in March (+655,000). (BLS JOLTS, May 5) Initial claims are still running 190–220K weekly, with continuing claims at 1.766M, a two-year low. (DOL ETA Weekly Claims) Those data points are real. They are also stale, they describe the March-April labor market, before the latest gas price spike, before the May 12-13 CPI/PPI repricing, before the financial conditions tightening that’s about to happen as mortgage rates rip back up.

My read: the labor market is following the typical late-cycle slowdown pattern. The order of operations is: participation falls → hours fall → part-time-for-economic-reasons spikes → claims rise → headline unemployment moves.

We’re already three steps in.

The bond market will likley soon acknowledge this labor weakness, and then the Fed will cut.

Nashville Corner: The Massive Oracle Development is Materializing

While you I have been arguing about inflation prints and labor participation rates, the single largest commercial-real-estate story in Nashville quietly moved forward this week.

On May 13, Oracle unveiled the renderings of its planned pedestrian bridge across the Cumberland River. Designed by London firm Foster + Partners, the people who built Apple Park and the Hong Kong airport.

It will be a steel cable-stayed structure, 863 feet long, 16 feet wide, with a cast-in-place concrete deck. It connects Taylor Street in Germantown to Cowan Street and River North Boulevard on the East Bank. (Foster + Partners renderings)

Construction begins August 2026. Two-year build. (WSMV, May 14)

What the Bridge Actually Is

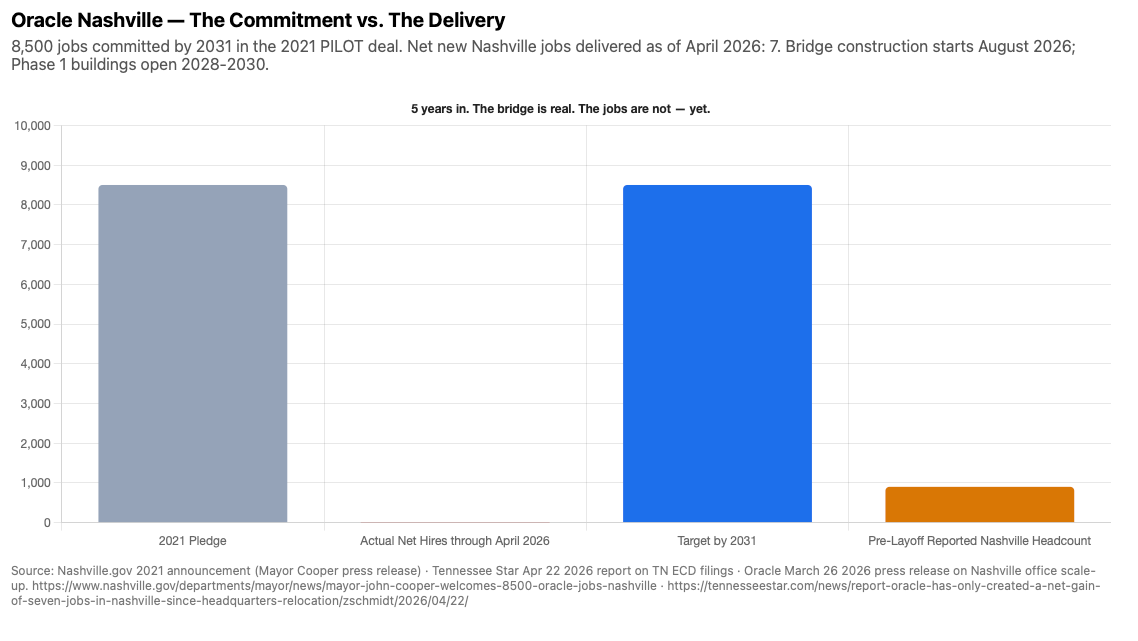

The pedestrian bridge is not a vanity infrastructure project. It is a publicly mandated obligation that Oracle agreed to as part of the 2021 $175 million deal.

Under that deal, Oracle gets a 50% property tax rebate for up to 25 years on the East Bank campus, capped at $175M.

In exchange, Oracle commits to:

$1.2 billion in capital investment (Nashville.gov, 2021)

8,500 jobs at an average salary of $110,000 — by 2031

$175 million in public infrastructure: the pedestrian bridge, brownfield remediation, a sewer pump station, and a riverfront public park

Tennessee also kicked in $65 million in state grants. Total subsidy package: ~$240M public dollars against a then-projected $1.2B private investment.

The bridge is the most visible piece of the public-infrastructure obligation. When Oracle files for the bridge permit and starts construction in August, they are putting steel on the ground that they cannot easily walk away from.

That’s the signal.

What’s Actually Built (and Not Built)

It's also important to take an accounting of what has and has not happened in the deal.

Here’s the Oracle Nashville scorecard as of mid-May 2026:

Done:

70-acre site assembled along the East Bank. (Granthammond Real Estate)

Demolition permits filed for 500,000+ sq ft of existing industrial buildings.

Active site clearing underway. (The Real Deal, January 2026)

Metro Council approved updated zoning in April 2026. (Fox 17)

Oracle signed a 116,000 sq ft interim lease at the Neuhoff District (1320 Adams St) in March 2026, putting employees right across the river from the future campus.

Foster + Partners pedestrian bridge renderings unveiled (May 13).

In progress:

Phase 1 buildings under design — first opening targeted for 2028 to 2030 (sources disagree on the exact year). (HereNashville)

Bridge construction starts August 2026; targeted completion 2028.

Nobu-branded luxury hotel planned for the campus.

Not yet:

The 8,500 jobs! (More on this below).

Full 2.7 million sq ft of office, retail, and hospitality. (Master plan timeline: 2031.)

The Project May be Lagging Behind

In April 2026, the Tennessee Star reported — based on filings with the Tennessee Department of Economic and Community Development — that Oracle has created a net total of 7 jobs in Nashville since the 2021 headquarters relocation announcement. (Tennessee Star, April 22, 2026)

Seven jobs.

Against a commitment of 8,500.

Now — the picture is more nuanced than that headline.

Oracle reported approximately 901 Nashville-based jobs before its March 31, 2026 global layoff round (which cut ~30,000 Oracle employees worldwide — the largest workforce reduction in the company’s 49-year history). (Axios Nashville, April 13) So Oracle clearly has more than 7 people in Nashville. But the net gain of jobs attributable specifically to the relocation commitment — the number the state tracks for deal compliance — is 7.

So the gap between the commitment and the delivery is large. Larger than the boosters acknowledge.

What This Means for Real Estate Investors

Three takeaways for those of us actually deploying capital:

One — the long-term East Bank / Germantown thesis is intact, but the timeline has slipped. Germantown median home prices are sitting around $666,750, essentially flat YoY (−0.25%). (Houzeo) That is not a market pricing in 8,500 Oracle jobs landing nearby in 2026 or 2027. The market is pricing in eventual Oracle delivery on a 2029-2031 horizon. If you bought Germantown in 2022 expecting a 2024-2025 Oracle-driven price pop, you’ve been underwater on your thesis for two years.

Two — the bridge starting construction in August 2026 is the inflection point. Steel in the ground is harder to walk away from than a press release. Once that bridge breaks ground, the East Bank development thesis has a physical anchor. The Phase 1 buildings opening 2028-2030 are still the main event, but the bridge is the visible signal between now and then that the deal is real.

Three — the “tax incentives buy guaranteed jobs” model is on trial here.Nashville bet $175M of foregone tax revenue plus $65M of state grants on Oracle hitting 8,500 jobs. Five years in, the delivered count (net) is 7. Even if Oracle hits 4,000 jobs by 2031 — half their pledge — Nashville will have made a defensible deal because of the $1.2B capital investment that materially raises East Bank land values. But Nashville taxpayers should not pretend the 8,500 number is a base case. It is a ceiling.

Counterpoint: Oracle’s CEO

Oracle’s CEO Safra Catz has said repeatedly through 2025 and 2026 that the company is doing a strategic AI pivot and that the Nashville campus is positioned as the operational hub of Oracle’s healthcare-AI and cloud-AI businesses.

The Oracle March 26, 2026 press release on scaling Nashville offices specifically called out cloud engineering, software development, and AI product roles as the growth areas. The March 31 layoffs hit Cerner consulting and ERP sectors of the company, not the AI buildout teams.

If you read the layoffs and the campus expansion together, the implication is: Oracle is shedding legacy headcount in Austin and other locations while building net-new in Nashville for AI-specific roles. Under that read, the next 12-24 months could see Nashville hiring accelerate dramatically, not stall further.

The bridge is also a 24-month build that requires Oracle to keep paying contractors, designers, and Foster + Partners regardless of macro conditions. You don’t engage one of the most expensive architecture firms in the world to design a pedestrian bridge if you’re hedging your bets on whether to follow through.

So the optimistic case is real: AI pivot + capital commitment + bridge construction = an Oracle that delivers 5,000-7,000 of the 8,500 jobs by 2031, even if not all of them.

The Verdict: I think 3,000-5,000 jobs by 2031 is the realistic range. 8,500 is a stretch.

But 3,000-5,000 well-paid tech jobs in the East Bank corridor, combined with $1.2B of capital investment, will be explosive for Nashville real estate values. The bridge announcement this week is the data point that converts the Oracle story from “deal on paper” to “deal under construction.” The campus itself opens 2028-2030.

The project is looking very positive for the Music City.

A Quick Ad Break — Advertise to 40,000+ Weekly Skeptical Investor Readers

Real estate, finance, and economic decision-makers read this newsletter every Sunday morning. If your product, service, or platform serves them, get in touch.

Reply to this email or reach out at andreas.mueller01@gmail.com.

My Skeptical Take

This week’s through-line is both optimistic and contrarian.

The bond market is already pricing in no Fed cuts in 2026 on the back of an inflation worry that is fundamentally an energy story, which is almost by definition temporary. But the market is offsides, folks read the inflation print and ignored the labor print sitting right next to it.

Perhaps the market is merely testing the new Fed Chair Warsh, as it has pretty much every Fed Chair in history? Today could be his first day on the job.

Either way, labor should be our and the Fed’s primary focus.

Labor force participation fell to 61.8% — the lowest since October 2021. The fifth straight monthly decline. Workers forced into part-time jobs spiked +445,000 in a single month to 4.9 million. Real wages fell.

A cut into high inflation is not historically unprecedented.

In 2008, when I was working on Capitol Hill as a younger man, Ben Bernanke cut rates into inflation that was running 5.6% YoY in July, because the labor market was breaking.

In 2001, Greenspan cut into a CPI running 3.4% because the economy was rolling over. The Fed cuts when labor cracks, not when inflation behaves.

The lesson of every recent cycle is that the rate-cut catalyst is labor, not inflation.

The bond market just front-ran the wrong catalyst.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

—

P.S. Want to level up your real estate game?

You can consult with me, The Skeptical Investor! Get professional advice from someone who actually owns, operates, and brokers real estate.

Want to Grow? - Get clarity on how to grow your business or scale.

Stuck? - Get answers to your problem, let's hop on the phone and figure it out.

No "guru" trying to sell you an expensive course. No BS. No fluff. Only results.

I'll give you my frank, brutally honest advice. Book a call with me today.

It’s 2026. Be an owner.

Schedule your 1-on-1 call now.