Eggs Are Cheap Again. Electricians, Not So Much.

Construction needs 349,000 more workers this year. Here’s what a permanent labor shortage does to supply, replacement cost, and rents.

Today’s Read Time: 8 minutes

This week, we’re talkin’ the economy is growing faster than the economists gave it credit for, eggs are back near their pre-bird-flu price, and electricians are the new diamonds. The country is short hundreds of thousands of skilled tradesmen, and the gap is growing. Real estate up.

Let’s get into it.

Today’s Interest Rate: 6.53%

(👇 .05% from last week, 30-yr fixed mortgage)

Rates barely moved, even after Thursday’s inflation reading came in hot.

The Weekly 3 in News:

The economy grew faster than expected. Q1 GDP was just revised up to +2.1%, up half a point from the prior estimate, mostly on softer imports (BEA). Steady growth, not great, not bad.

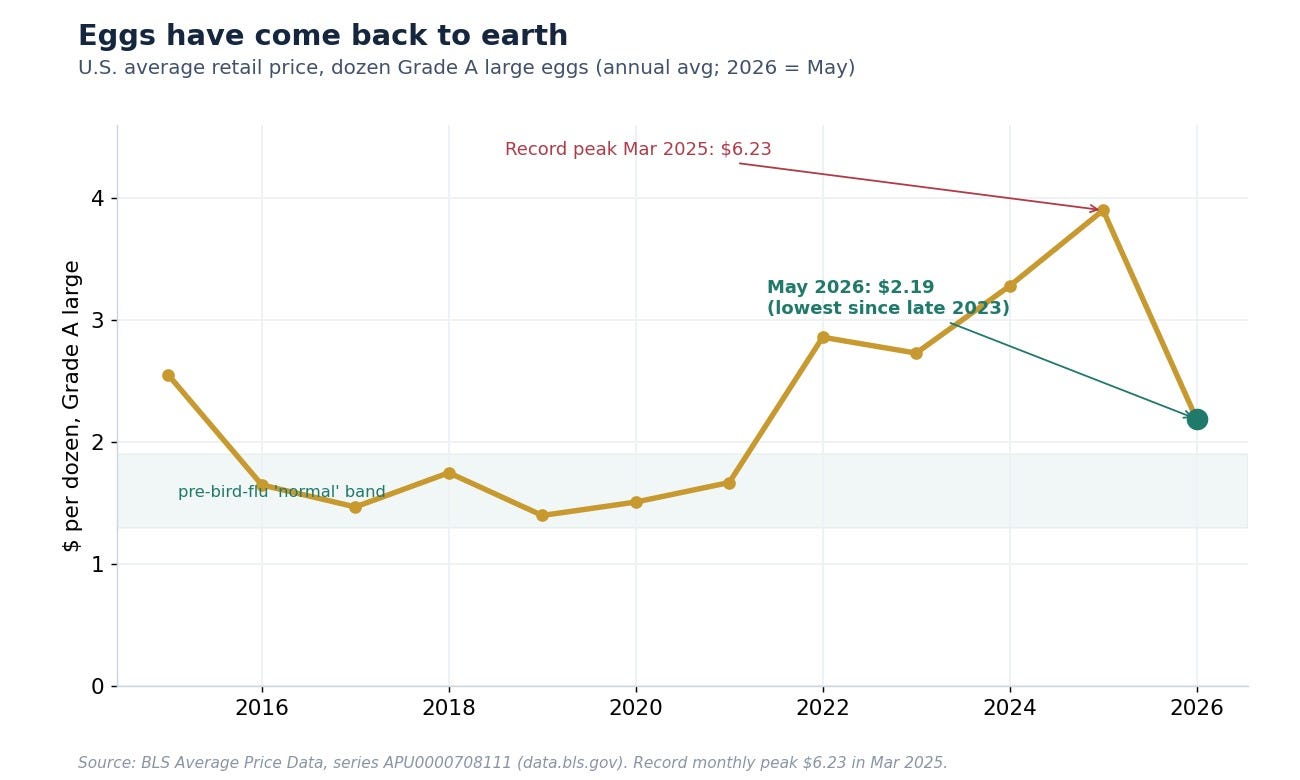

Eggs have come back to earth, cheapest since 2023. A dozen eggs averaged $2.19 in May, down about 2.6% from April and more than 50% off this year’s record peak of $6.23 in March 2025 (BLS). Why? The bird-flu flock the was culled has rebuilt, and producers have swung from shortage to oversupply (CNBC). Fresh Example: Whole Foods has my favorite eggs on sale, all month.

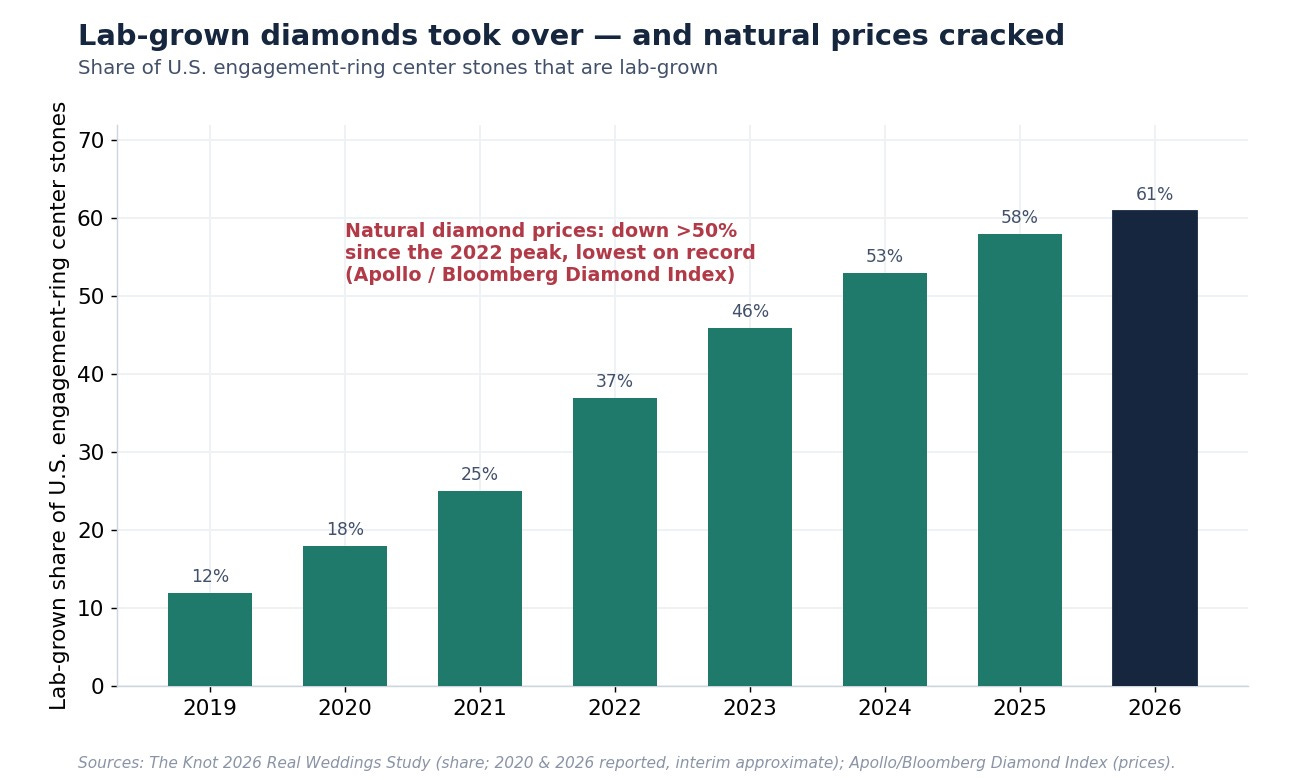

3. You know what’s not inflating? Diamonds. Prices are down more than 50% since their 2022 peak and sit at the lowest level on record (Apollo/Bloomberg Diamond Index). The cause? Folks are good with the manmade stuff now. Lab-grown stones now make up about 61% of U.S. engagement-ring center stones, up from roughly 18% in 2020 (JCK / The Knot), and they retail for a fraction of the price. De Beers’ owner, Anglo American, took a $3.7 billion loss in 2025 on the back of repeated De Beers write-downs and is trying to sell the business (MINING.com).

Why open a real estate letter with eggs and diamonds?

Keep reading…. :)

Oh and…

A Few Fun Things Happening in Nashville This Week

Let Freedom Sing! Music City July 4th — downtown, Friday July 3 and Saturday July 4. Nashville’s free, five-stage Independence Day blowout, this year tied to America’s 250th. The lineup runs from Boyz II Men to Brothers Osborne to Nick Jonas, capped by what the city bills as its largest-ever fireworks and drone show (Visit Music City). If you own short-term rentals near downtown, this is one of your highest-occupancy weekends of the summer.

New tables at Nashville Yards. Two notable openings worth a reservation: Prime + Proper, a modern steakhouse, and Earls Kitchen + Bar, both now open in the Nashville Yards district (Nashville Guru). The dining scene keeps following the corporate campuses.

US Labor Market Not Breaking

The labor market is cooling, but only a little and slowly, and not in the way the doom crowd online and the major news outlets keep predicting.

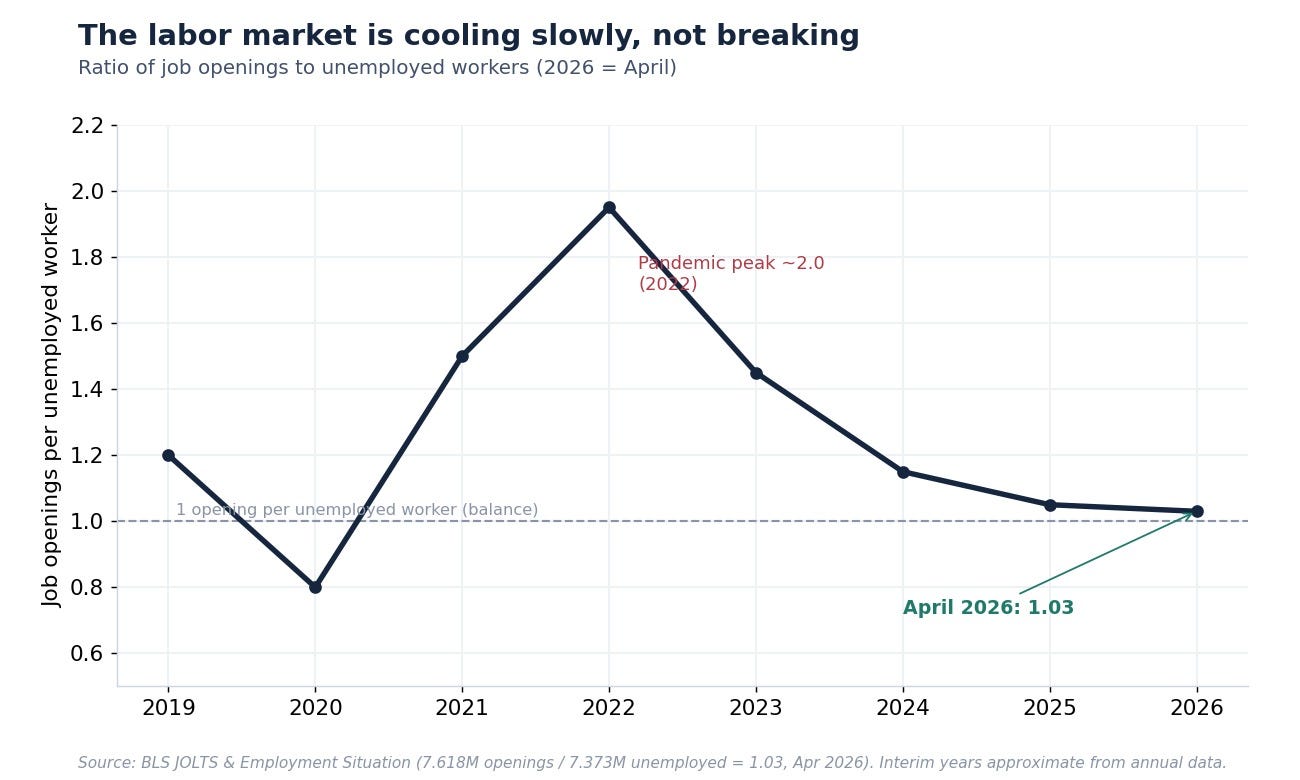

May payrolls added +172,000 jobs, and unemployment held at 4.3%, where it has sat in a tight band since last summer (BLS). Job openings actually jumped back to 7.6 million in April, which works out to roughly 1.03 openings for every unemployed worker, about the pre-pandemic norm (BLS JOLTS).

We are not at the white-hot 2022 peak, but we are also nowhere near the cliff.

The people losing jobs are taking a little longer to find the next one, which is what a soft landing looks like from the inside.

Now, last week I wrote about the 1961 “automation jobless” panic and how every generation convinces itself that this time the machines really will take all the work. This time is no different and it is my view is that AI is about to become a job accelerator, lifting both productivity and, eventually, headcount. I am extremely skeptical of the narrative that AI will lead to net job loss. And we are just starting to see this filter through the real economy.

Let’s start with the productivity side, with hard data.

US Labor Productivity is UP

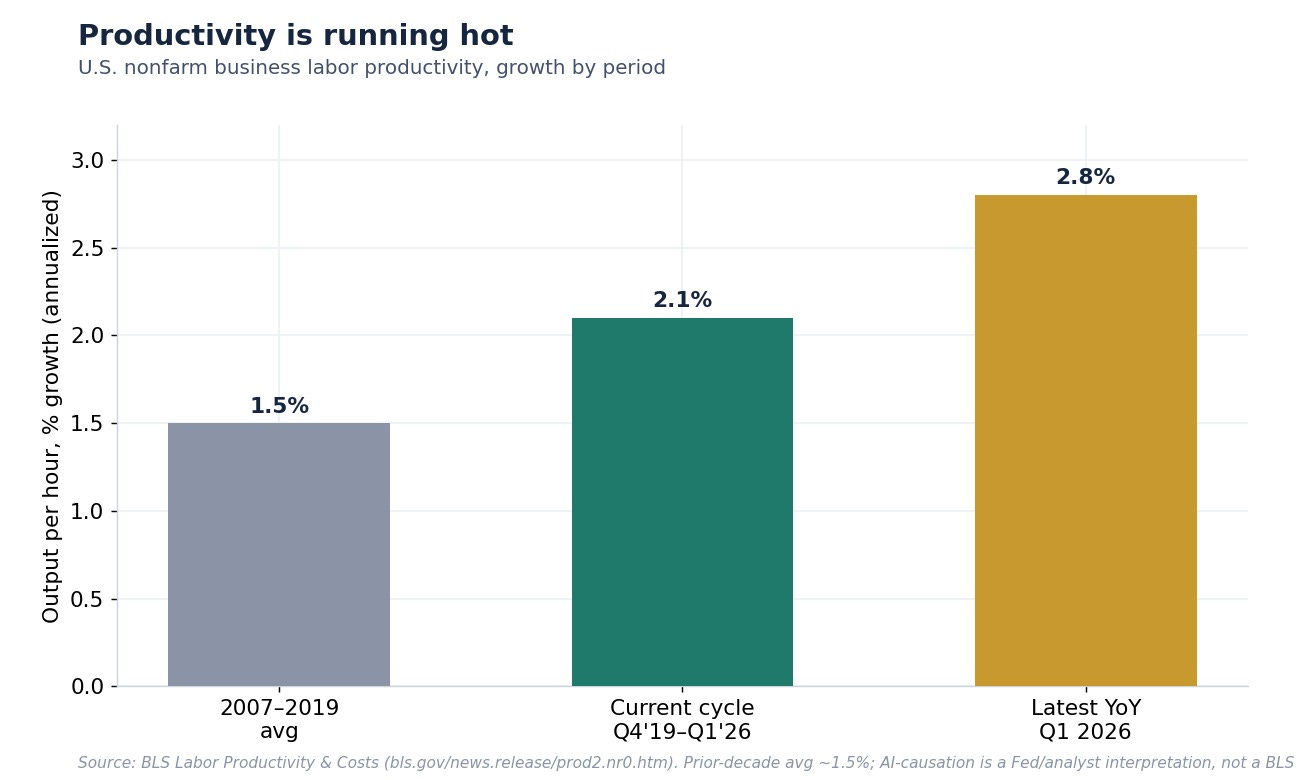

U.S. labor productivity grew 2.8% year-over-year in Q1, and the current business cycle has averaged about 2.1%, well above the roughly 1.5% pace of the 2007–2019 decade (BLS). Studies out of Stanford and MIT looked at thousands of customer-support agents, found generative AI lifted output about 14% on average, and around 30% for the least-experienced workers (NBER). AI is not replacing those agents. It is making the newest ones nearly as good as the veterans, fast.

A Bolder Call

On the question of whether AI is destroying jobs in aggregate, the best evidence so far says no. The New York Fed studied job postings around ChatGPT’s launch and found no clear divergence between AI-exposed and non-exposed roles. A Federal Reserve Board study of company hiring found AI adoption was associated with neither net job gains nor losses.

Compare this with the tech coming out party of the last century.

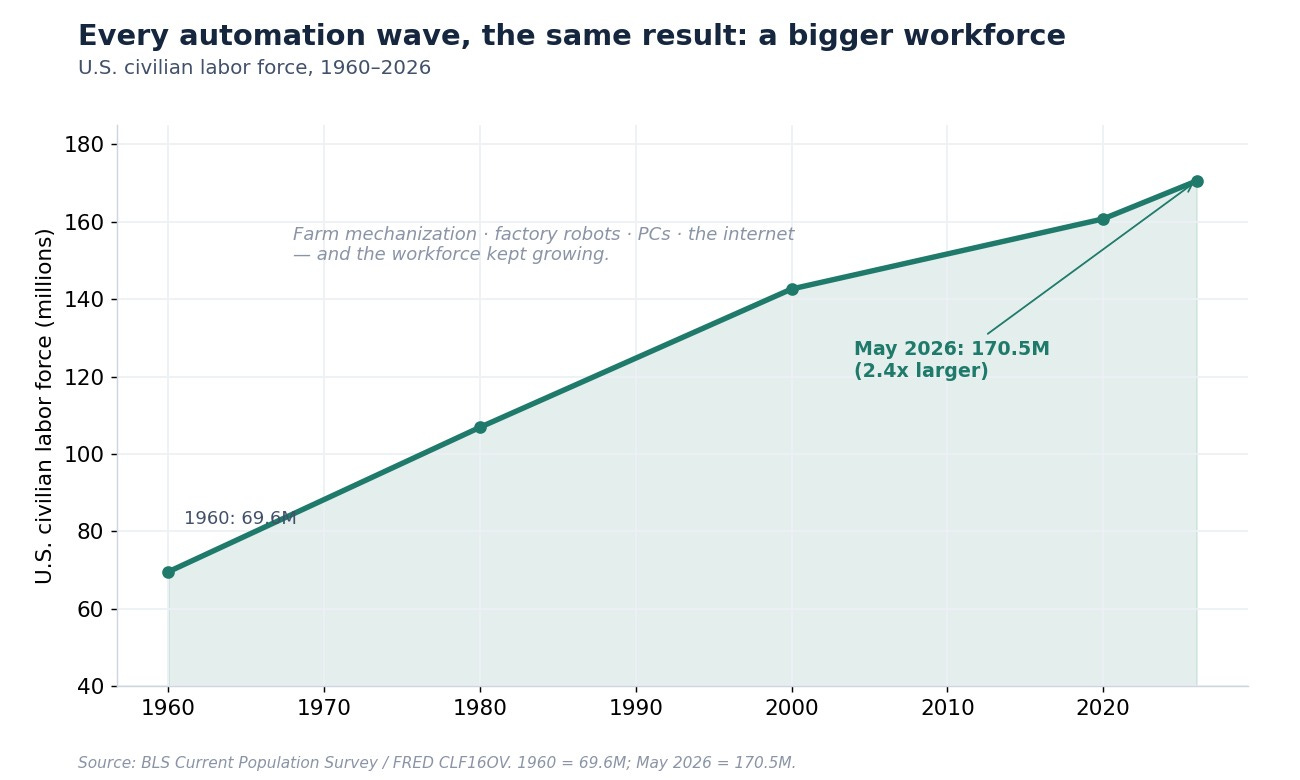

In 1960 the U.S. civilian labor force was about 69.6 million people. Today it is 170.5 million (BLS), even after we automated away the farm, the factory floor, the typing pool, and the telephone switchboard. The workforce did not shrink. It multiplied by two and a half. Every time we made human effort more productive, we found more for humans to do, and the things they did were better-paid than what came before.

The steelman: where the AI-optimists could be wrong

I’d be doing you a disservice if I only argued my own side (which is right, of course :)

The most rigorous warning sign comes from Stanford too, it’s “Canaries in the Coal Mine” study, which used real payroll data and found a 13% relative decline in employment for workers aged 22 to 25 in the most AI-exposed jobs since late 2022, with entry-level software roles down around 20%. If AI eats the bottom rung of the career ladder, you do not feel it in this year’s unemployment rate. You feel it in five years, when there are no mid-career workers because nobody got to start. Separately, the outplacement firm Challenger has tracked 87,000-plus layoffs attributed to AI so far in 2026, already more than all of last year (Challenger report).

I take that seriously.

I’d also note, in the spirit of skepticism, that many companies appear to prefer blaming “AI” for layoffs because it sounds better to investors than “we over-hired,” so the Challenger figure is probably inflated. And the entry-level softness may be as much about a frozen white-collar hiring market as about the machines. But I won’t pretend the displacement signal is zero.

My bet is that it stays at the edges, and the productivity boom pulls total employment up the way it always has. That is a bet, not a certainty.

Why a real estate investor should care:

Productivity growth is the roaring engine under wage growth, household formation, and rent. A more productive economy can afford higher rents without breaking the tenant. And if I’m right that AI grows the pie rather than shrinking it, the demand side of housing stays healthy for a long time. That is a very positive backdrop.

Now, here’s the supply side, and it’s even more interesting.

A quick ad break…T-Mobile

T-Mobile - Smarter, Faster Networks for Serious Teams

For years, enterprise leaders have compromised on connectivity, battling dead zones and rigid networks. Now, T-Mobile for Business is rewriting the rules. They introduced SuperMobile—a next-gen solution engineered to deeply transform how your enterprise runs, scales, and secures its data.

With SuperMobile, your teams get real-time, intelligent performance via the first-ever nationwide network slice built specifically for business.

Need remote reliability? They deliver seamless smartphone connectivity anywhere via the world’s largest satellite constellation. And because CFOs and CISOs demand compliance, they have embedded robust encryption and advanced device authentication directly into the core.

Stop letting siloed, legacy networks slow your big ideas down. Move forward with the advanced 5G connectivity your business deserves.

The Deep Dive: We Are Running Out of People Who Can Build

Like diamonds and eggs show us, when we can manufacture something at scale, whether that is a million year old protein or a new gemstone, the price falls.

Hard.

The things that stay expensive are the things we don’t.

In real estate, that rare commodity is the…journeyman.

We just don’t have enough skilled tradesmen and even fewer are in the pipeline.

Every housing-shortage story you read blames the same suspects: zoning, interest rates, land costs, lumber. All real. All worth discussing. But there is a constraint that gets a fraction of the attention and may matter more than any of them over the next decade. We do not have enough skilled workers to build the things we say we want to build.

This is getting worse.

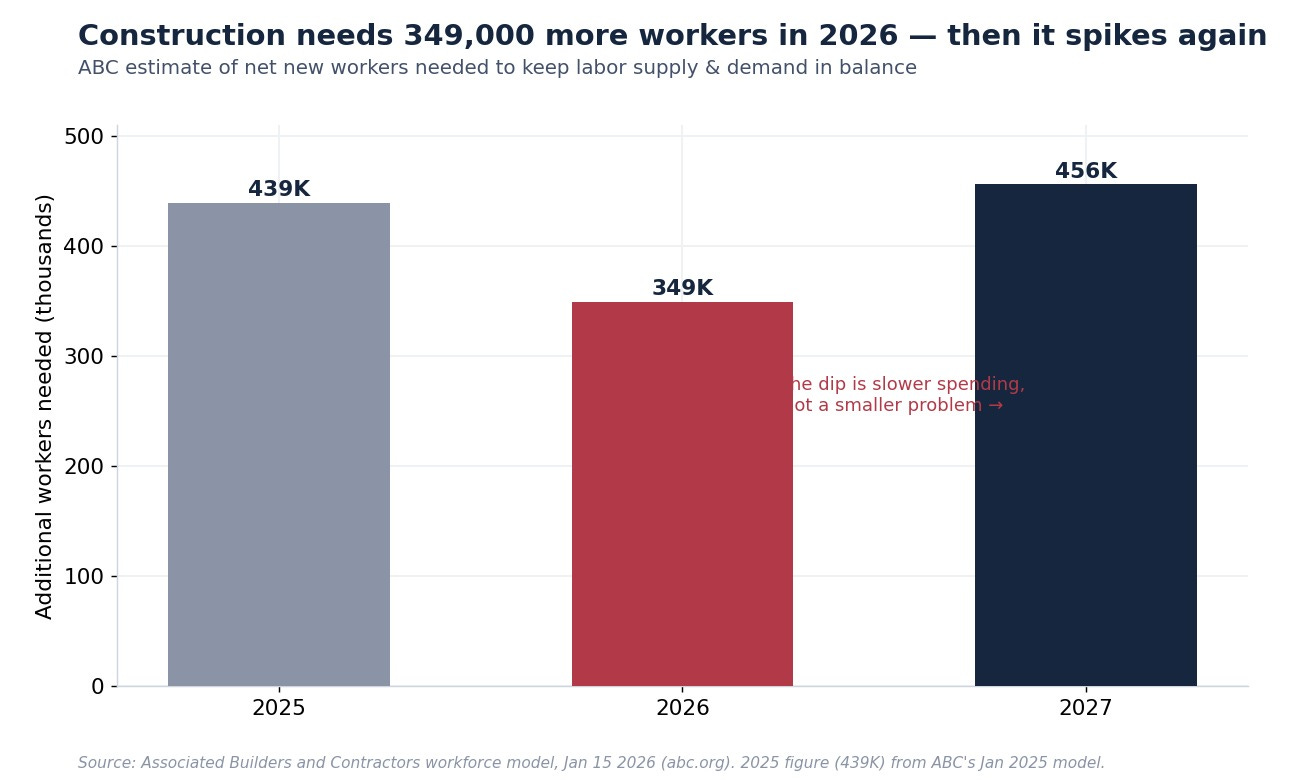

The Associated Builders and Contractors estimates the construction industry must attract 349,000 additional workers in 2026 just to keep the supply and demand for labor in balance (ABC). That is actually down from 439,000 in 2025, which sounds like progress until you read the fine print: the gap shrank only because construction spending slowed. ABC already projects the need rebounds to 456,000 in 2027 as spending resumes.

Contractors I work with feel it on the job. In the most recent industry workforce survey, 92% of firms reported trouble finding qualified workers, 88% had open craft positions they could not fill, and worker shortages were the single most common cause of project delays (AGC). When nine out of ten builders say they cannot find hands, that is not a soft spot. That is the binding constraint.

ABC’s chief economist, Anirban Basu, notes that the majority of the 2026 worker demand comes from retirement, not growth. The industry is not mainly trying to staff up for new projects. It is trying to replace the people walking off the job for the last time. The median construction worker is now 42 years old (NAHB), and roughly one in five electricians is over 55.

This is a workforce aging toward the exit faster than it is being refilled.

Where the squeeze is tightest

Not all trades are short by the same amount. The crunch is worst in the licensed, can’t-fake-it specialties, and it is about to get worse because of one word: electricity.

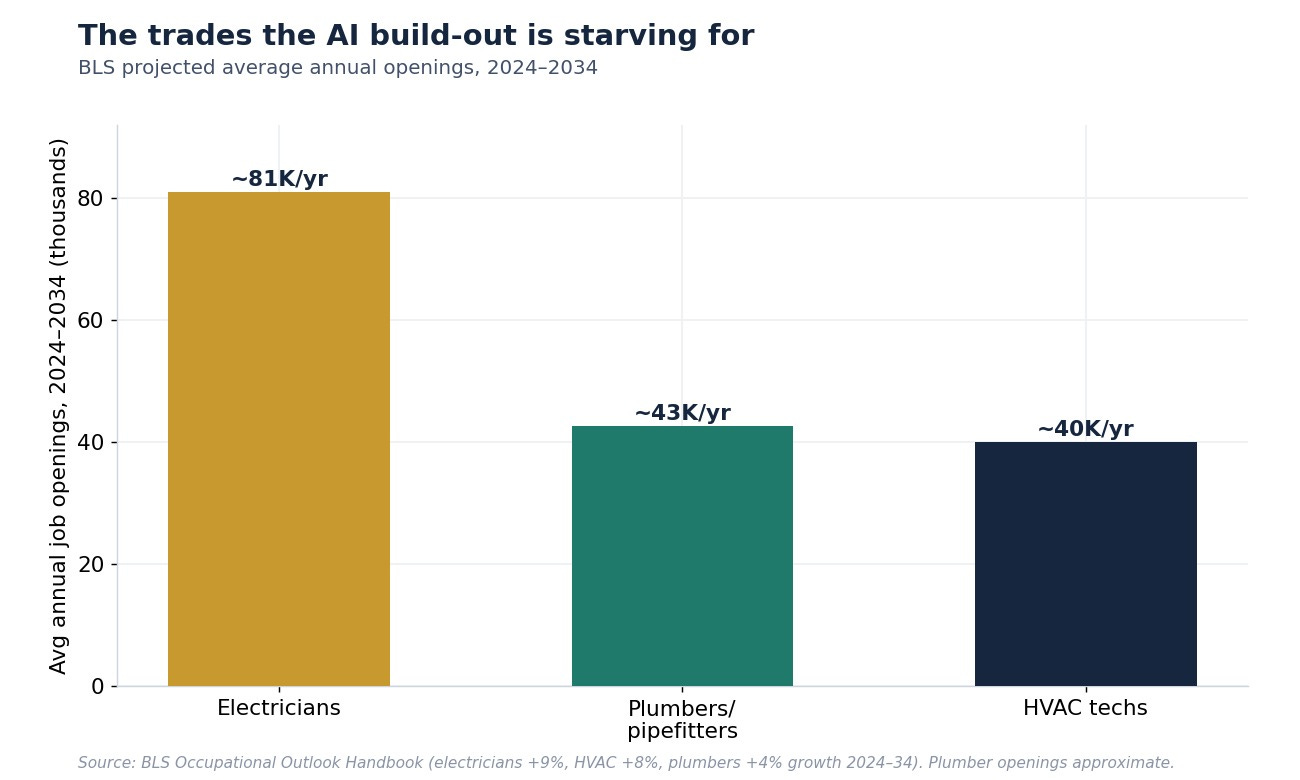

The BLS projects roughly 81,000 electrician openings every year through 2034, with 9% job growth, faster than the average occupation (BLS). HVAC technicians are close behind at 8% growth and about 40,000 openings a year (BLS). Plumbers and pipefitters round out the trio (BLS).

The AI Datacenter Buildout Effect

Ironically, while AI will help tradesmen companies be more efficient, the MASSIVE current data center build-out is makes this much worse in the short to medium term.

The data-center boom that everyone is treating as a software story is, on the ground, an electrician story. Hyperscalers compete for the same finite pool of licensed electricians that homebuilders and commercial developers need (CNBC, Fortune). A data center is, in cost terms, largely an electrical project wrapped in a building. When Microsoft and a Nashville apartment developer are bidding for the same crew, the apartment developer is going to pay more, wait longer, or both.

The technology we’re all betting will automate away jobs is, right now, creating a desperate shortage of exactly the human, hands-on jobs that can’t be automated.

You can’t prompt a chatbot to bend conduit, yet.

The immigration variable

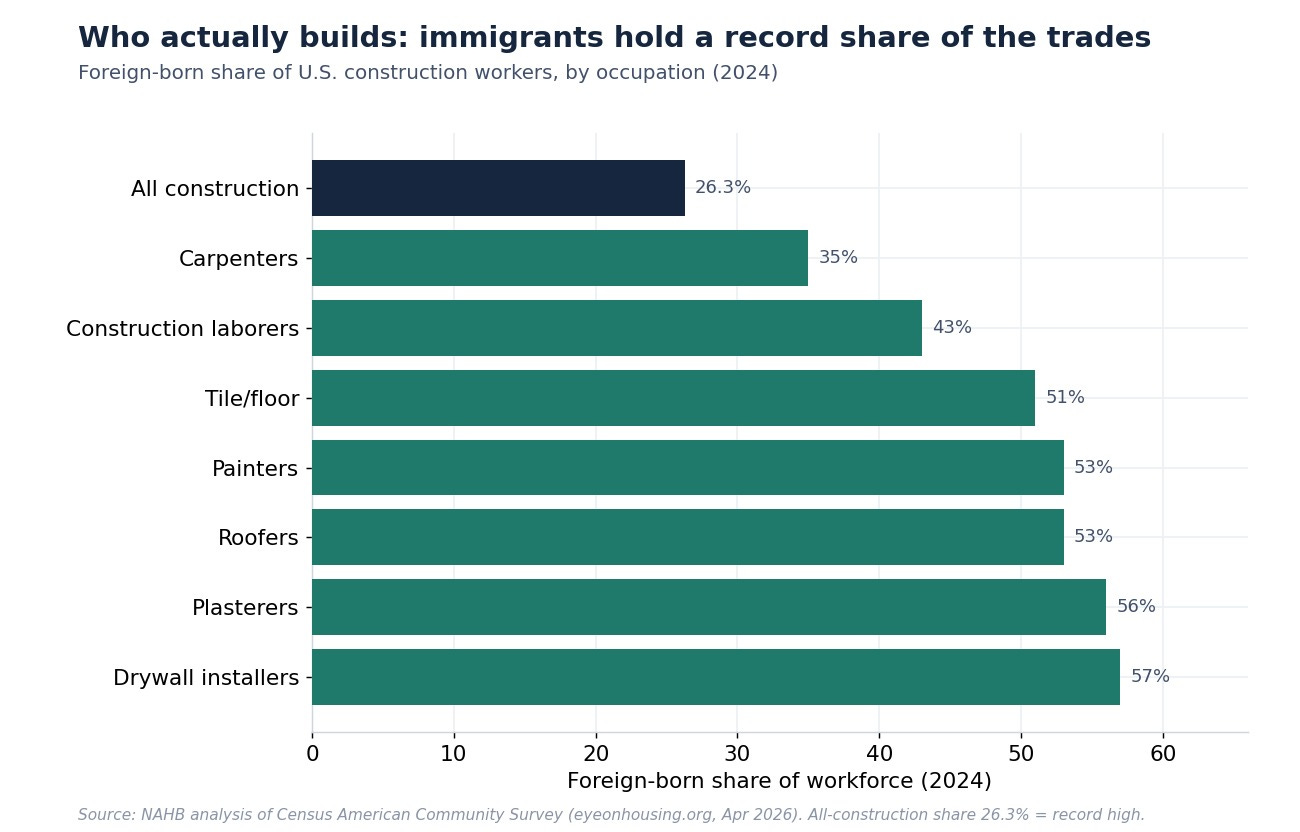

Immigrants make up a record 26.3% of the total construction workforce as of 2024, and roughly a third of the actual tradespeople (NAHB). In some trades the share is far higher: about 57% of drywall installers, 53% of roofers and painters, half of all tile and flooring workers.

This matters NOW, because the flow of new immigrant labor has slowed sharply, and 28% of contractors report that immigration enforcement has already affected their workforce in the past six months (AGC).

This is not political. As an investor, the fact is a large share of the people who physically build housing are foreign-born, that pipeline is narrowing. Tighter labor supply, meet tighter labor supply, means higher prices.

What it does to the only number you underwrite

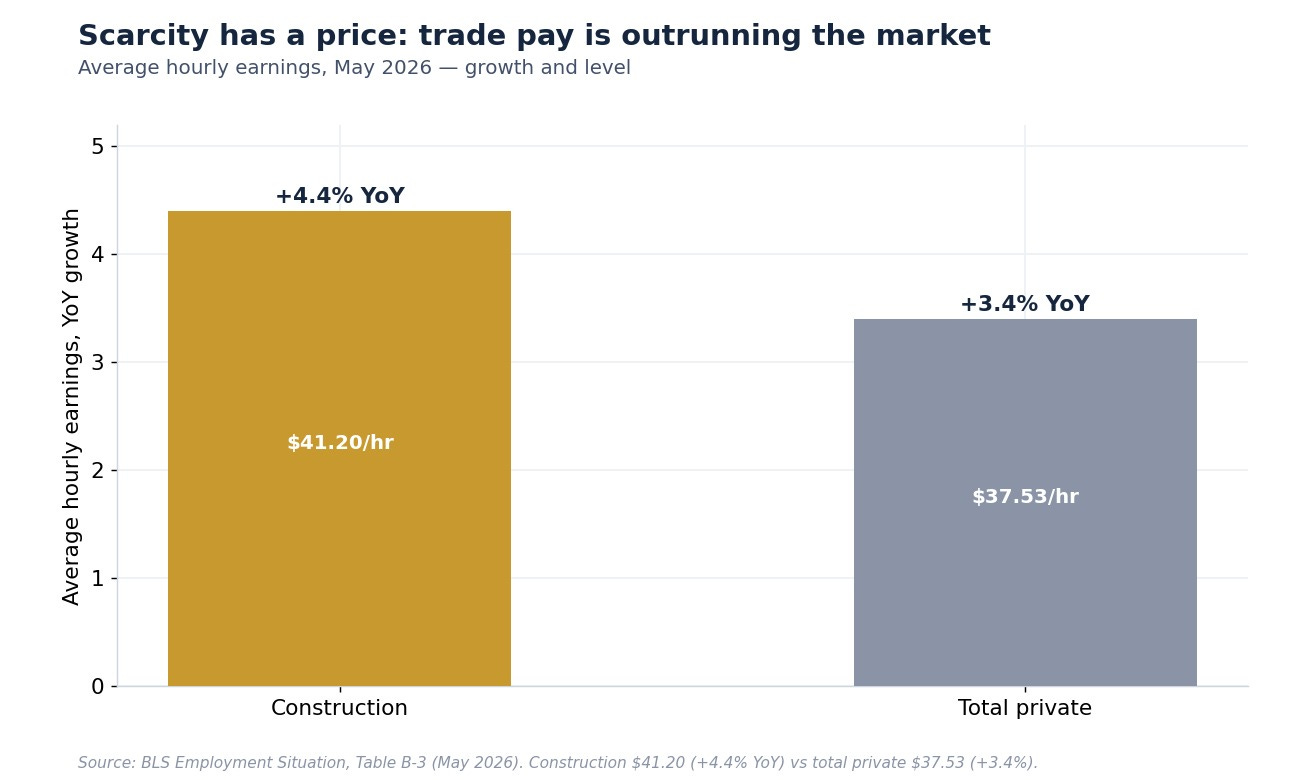

All of this shows up in one place on your spreadsheet: cost. Construction wages rose 4.4% over the past year, to about $41.20 an hour, outpacing the 3.4% gain for private workers overall (BLS). Skilled-trade pay is rising faster than the broader market, and it has been for a while.

On net, this is good news for anyone who already owns buildings. Rising labor costs raise the replacement cost of every existing structure. When it costs more to build the competing apartment across the street, two things happen. New supply gets harder to pencil, so less of it shows up, and the building you already own becomes more valuable relative to a world where anyone could cheaply build its twin.

A permanent labor shortage is a permanent governor on how fast supply can grow, and right now the brake is on.

Construction Employment Is the Signal for Recession

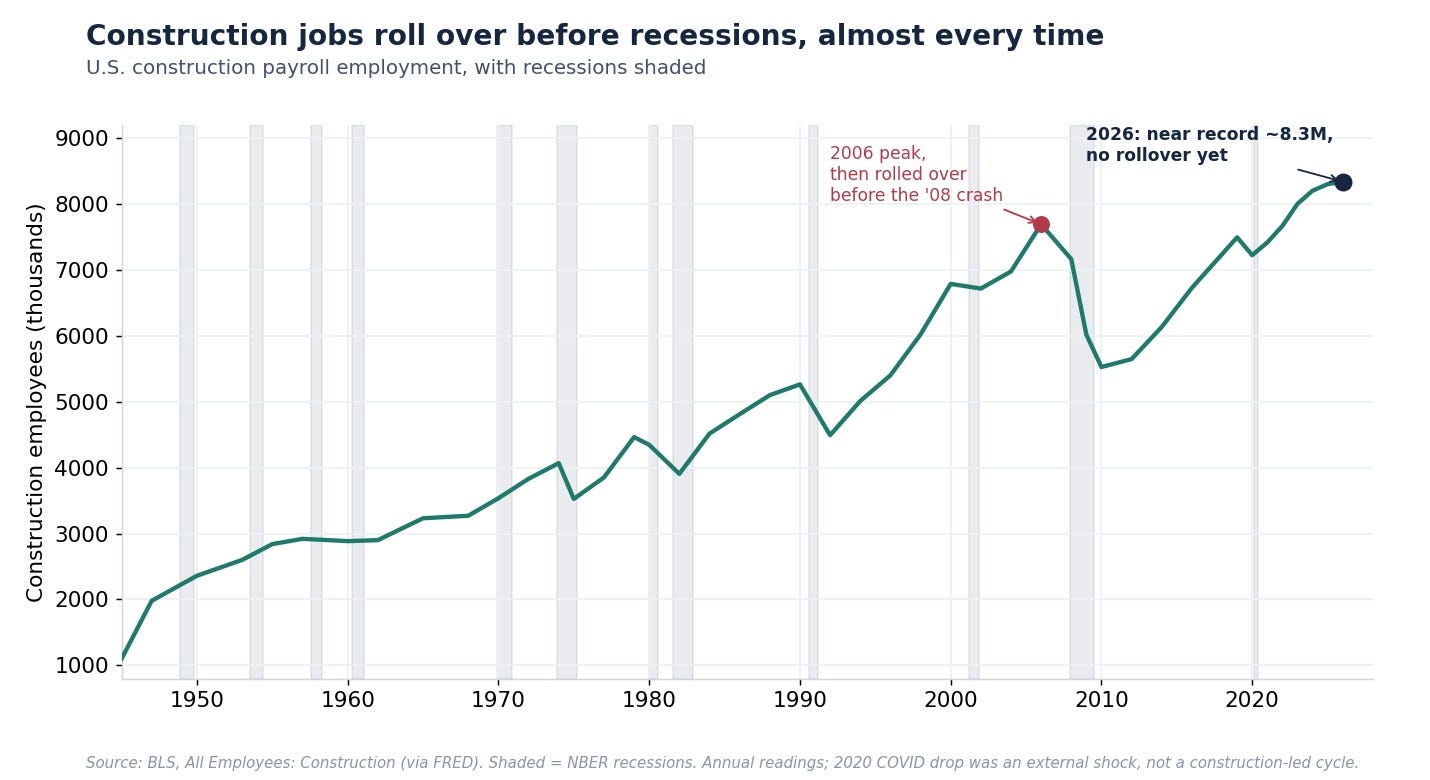

Construction employment does more than build houses: it forecasts the business cycle.

Going back to World War II, payrolls in the building trades have peaked and started falling before nearly every U.S. recession, then dropped hard once the downturn arrived. The Bureau of Labor Statistics put the pattern right in the title of a 2011 study, “Construction Employment Peaks before the Recession and Falls Sharply Throughout It.” The logic is intuitive. Builders commit capital and crews on their read of the next 12 to 18 months, so when they start trimming, they are telling you what they see coming.

The 2008 crash is the cleanest example: residential construction employment had already fallen about 11% before the recession was officially dated (BLS). It is not a flawless signal. It missed the 2020 shock, which arrived from a virus rather than the credit cycle, and it has thrown the occasional false alarm. But as cyclical tells go, it has a better track record than most of what gets airtime.

Which makes the current reading worth sitting with. Construction employment is parked near an all-time high, around 8.3 million (BLS), and it has not rolled over. Under the leading-indicator logic, that appears to be a quiet green light for the broader economy, and it squares with everything else in this issue: the reason builders are not shedding workers is that they cannot find enough to begin with. A labor shortage may turn out to be its own kind of recession insurance.

This is exactly the kind of second-order thinking I try to bring to every deal, and it’s the reason I built a tool to force myself to underwrite honestly. If you want to pressure-test how rising construction and replacement costs change a deal’s math, run a few scenarios through my DealLab analyzer. It underwrites a rental, BRRRR, or flip in seconds, with live mortgage rates, cap rate, cash-on-cash, DSCR, and a deal heat score. I just added an Advanced Mode for the pros who want to get into the weeds. It’s free, it’s in beta, and I genuinely want your feedback to make it better. Bookmark it. It will come in handy the next time a deal lands in your inbox.

A Quick Ad Break — Advertise to Skeptical Investor Readers

40k+ Real estate, finance, and economic decision-makers read this newsletter every Monday morning.

If your product, service, or platform serves them, you can advertise with us.

My Skeptical Take

We can grow a diamond in a lab now.

We can pump out eggs by the billion once the flock recovers.

We are teaching software to do a junior analyst’s first year of work in an afternoon.

Anything we can systematize, we eventually make cheap. That is the deflationary miracle of a productive economy, and it is mostly good news, especially when it puts a 137-year-old diamond cartel out of business.

But notice what stays expensive. A person who can climb into a 120 degree attic in July, read a load calculation, and wire a house so it doesn’t burn down. A framing crew that shows up at 6 a.m. and gets the deck right. The hands that actually build the thing. We have spent thirty years telling a generation of kids that those jobs were beneath them, and now we are 349,000 workers short and writing checks that grow 4.4% a year to the ones who stayed.

For an owner of real estate, the cost of creating new competition for your building keeps rising as building gets harder, and the people required to create it keep getting scarcer.

Mike Rowe, who has spent more time than anyone making the case for the trades, put the cultural root of the shortage better than I can:

“We’ve waged war on work. We’ve declared that a four-year degree is the only path to success, and we’ve treated the skilled trades like a vocational consolation prize. The skills gap is just a reflection of what we decided to value.”

The gap is real. The buildings are getting more expensive to replace. And the people who own the ones that already exist, and who keep their numbers honest while everyone else chases the shiny thing, are positioned about as well as I’ve seen in this cycle.

But eventually, we need to get back to building more than datacenter in this country.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-

Need some personal help with your real estate portfolio?

You can consult one-on-one on the phone with me, The Skeptical Investor!

Get professional advice from someone who actually owns, operates, and brokers real estate. Not just some partner in a fund making money off others.

Want to Grow? - Get clarity on how to grow your business or scale.

Stuck? - Get answers to your problem, let’s hop on the phone and figure it out.

No "guru" trying to sell you an expensive course. No BS. No fluff. Only results.

I'll give you my frank, brutally honest advice. Book a call with me today.

It’s 2026. Be an owner.

Schedule your 1-on-1 call now.